A Refereed Monthly International Journal of Management

SERVICE QUALITY AND CUSTOMERS’ SATISFACTION IN HDFC BANK

Author

|

(A Study of Selected Private Rural Banks in Karimnagar District of Telangana State)

Dr. E. HARI PRASAD & Prof. G. V. BHAVANI PRASAD

|

Abstract

In the present competitive economy banking sector has been facing dynamic challenges

in concerning both customer base and performance. The indispensable competitive

strategic role of this sector is vital one in managing the customers. Providing

service quality is highly significant function of service industry in today’s

competitive environment. Service quality is the excellent strategy and plays a key

role in service sector in general and banking sector in particular to satisfy the

customers’ needs and retain them. The present study aims at assessing the

service quality that delivered by the banks in rural areas, using SERVQUAL model.

Key Words: Rural Banks, Regional Rural Banks, Service Quality,

Service quality gaps, Expectations and Perceptions.

Introduction

In many countries service sector plays dominant role in the markets. According to

(Kotler, 2003), in the US economy, nearly 80 per cent of the employment opportunities

provided and 76 per cent of the GDP contributed by the service sector. In India

also service sector playing greater role in the nation’s economy by contributing

nearly 64 per cent of the GDP, having higher share in exports, 42 per cent of total

exports from India, and providing high number employment opportunities. This indicates

that the growing importance of the service sector. That is the reason why, companies

well recognized the need for the better service quality and are looking for ways

to perform better and attract and retain their customers in a high competitive manner

(Wang. Y., 2003). Many researchers have been focused on this area of service quality

for the last few years and recognized as one of the most important strategy of the

business firms in the service sector to improve financial as well as marketing performance.

(Newmn, 2001) Service quality has been defined as the degree and direction between

customer service expectations and perceptions. Perceived service quality is defined

as how well a service satisfies the expectations of customers. Service quality has

an impact on profitability and costs, as service quality influences customer satisfaction;

it impacts customer retention, reduces costs and increases profitability.

- Associate Professor, Dept. of Business Management Vaageswari College of Engineering

– Karimnagar, Telangana State, hariesharma@gmail.com,

+91 9490072311.

- Principal, Dept. of Business Commerce and Business Management, Kakatiya University

– Warangal, Telangana State bhavaniprasadgv@gmail.com,

+91 9848193906.

It is, thus, service quality has been identified as a key determinant of the intention

to use a service, and has, therefore, been extensively under study.

Importance of Service Quality

Service quality is considered as the most critical determinant of competitiveness

for establishing and sustaining satisfying relationship with customers (Lewis, 1989).

Business firms including banks have recognized the fact that the only one best way

to manage the competition is the quality differentiation. Advance technology, customer

oriented corporate culture, a well designed service-system and excellent information

system are the major factors that decide the superior quality of service of an organization.

Providing excellent service quality and maintaining the high customer satisfaction

is the important issue and the challenge facing contemporary service industry (Hung,

2003). Thus Service Quality is an important subject in both public and private sectors

business firms and service industries. Banking sector is not an exception to this.

Before independence the banking system in India was in private sector and in very

weak position. To strengthen the banking system then government established Reserve

Bank India (RBI) in 1935 and empowered to regulate banking companies by issue of

directive, inspection, amalgamation, mergers etc. Major action was taken 1949 by

passing the Banking regulation Act which was very important in respect of structural

reforms in the banking sector. This act had given extensive regulatory powers to

RBI over the banks in India. Nationalization of banks was another major step of

the government (14 banks on 19th July, 1969 and 6 banks on 15th

April, 1980) to constitute the public sector banks. These public sector banks occupied

a vital role in Indian economy in general and banking sector in particular. Government

implemented many social welfare schemes through these banks. Prior to globalization

there was very little competition in the banking sector and the public sector banks

played dominating role in terms of size of assets? Due to changing global scenario,

the government recognized the need to introduce reforms to make banking industry

more competitive. Thus, the government had made policy changes like deregulation

of interest rates and dilution of consortium lending requirement. Moreover, banking

sector had been opened up to the private sector. With this, new banks have been

set up in private sector, called as new private sector banks, foreign banks have

entered the Indian banking sector and existing banks in private sector (old private

sector banks) changed their level of operations. All these increased the competition

among the banks and efficiency of the banking industry.

Survival of banks, in heavy competition, depends upon how the banks are providing

quality services to their customers. Service quality is a comparison of expectations

with performance. From the viewpoint of business administration, service quality

is an achievement in customer service. It reflects at each service encounter (Bhatia,

Assessment of Service Quality in Public and Private Sector Banks of India with Special

Reference to Lucknow City). A customer's expectation of a particular service is

determined by factors such as recommendations by peers, personal needs and past

experiences. The expected service and the perceived service sometimes may not be

equal, thus leaving a gap. The service quality model or the ‘GAP model’

developed by the authors- Parasuraman, Zeithaml and Berry at Texas and North Carolina

in 1985, highlights the main requirements for delivering high service quality. It

identifies ‘gaps’ that cause unsuccessful delivery of service. Customers

generally have a tendency to compare the service they 'experience' with the service

they 'expect'. If the experience does not match the expectation, there arises a

gap.

Service Quality Dimension - Service Quality Gap Model (SERVQUAL)

The gap model (also known as the "5 gaps model") of service quality is an important

customer-satisfaction framework. In "A

Conceptual Model of Service Quality and Its Implications for Future Research"

(The Journal of Marketing, 1985), A. Parasuraman, VA Zeitham and LL Berry identify

five major gaps that face organizations seeking to meet customer's expectations

of the customer experience.

SERVQUAL is one the tools used in measuring the quality of services. According to

Buttle (1996), SERVQUAL is for the measuring and managing the quality of service.

Asubeonteng et al (1996) also intimated that the model is used to measure the quality

of service from the customer’s point of view. The originators of the model

are Parasuraman, Zeithamal and Berry. It was developed in 1985 but was polished

in their subsequent articles (Parasuraman et al 1988). The main aim of SERVQUAL

is to have a standard and a reliable tool that can be used to measure the quality

of services in different service sectors. Originally, those who developed SERVQUAL

introduced ten service quality dimensions or attributes. These are: 1. Tangibles,

2. Reliability, 3. Responsiveness, 4. Competency, 5. Courtesy, 6. Communication,

7. Credibility, 8. Security, 9. Access and 10. Understanding the customer.

Table – 1 Definition of Original Ten SERVQUAL Dimensions

|

Sl. No.

|

Dimension

|

Definition

|

|

1

|

Tangibles

|

Appearance of physical facilities, equipment personnel and communication materials.

|

|

2

|

Reliability

|

Ability to perform the promised service dependably and accurately.

|

|

3

|

Responsiveness

|

Willing to help customers and provide prompt service.

|

|

4

|

Competence

|

Possession of the required skills and knowledge to perform the service.

|

|

5

|

Courtesy

|

Politeness, respect consideration and friendliness of contact personnel.

|

|

6

|

Credibility

|

Trustworthiness, believability, honesty of service provider.

|

|

7

|

Security

|

Freedom from danger, risk of doubt.

|

|

8

|

Access

|

Approachability and ease of contact.

|

|

9

|

Communication

|

Keeping customers informed in language they can understand and listening to them.

|

|

10

|

Understanding the Customer

|

Making the effort to know customers and their needs.

|

|

Source: Zeithmal, Parasuraman and Berry, (1988) Delivering

Quality Service, New York, Free Press, p 21-22 (Modified)

|

|

Table - 2

|

|

Ten Dimension

(Original Model)

|

Five Dimension

(Later Model)

|

|

Tangibles

|

Tangibles

|

|

Reliability

|

Reliability

|

|

Responsiveness

|

Responsiveness

|

|

Competence

Courtesy

Credibility

Security

|

Assurance

|

|

Access

Communication

Understanding

the customer

|

Empathy

|

|

Source: Zeithmal, Parasuraman and Berry, (1988) Delivering

Quality Service, New York, Free Press, p 26.

|

However, in the 1988 article, these were pruned to five (Parasuraman et al 1988).

These are, 1. Tangibles, 2. Reliability, 3. Responsiveness, 4. Assurance and 5.

Empathy. Tangibility refers to the physical environment in which the service provider

operates. It comprises the physical facilities available, workers, and equipment

and communication materials. Reliability concerns the ability with which the service

organization can deliver the service dependably and accurately. Empathy on the other

hand, is about the special care and attention given to individual customers when

being served. Responsiveness is also the preparedness of the service provider to

assist customers and render as quick of prompt service as possible. Assurance too

is in connection with knowledge and the courteous attitude of staff and their ability

to instill, trust and confidence in customers.

|

Table – 3 Definition of Service Quality Dimensions

|

|

Sl. No.

|

Dimension

|

Definition

|

|

1

|

Tangibles

|

Appearance of physical facilities, equipment personnel and communication materials.

|

|

2

|

Reliability

|

Ability to perform the promised service dependably and accurately.

|

|

3

|

Responsiveness

|

Willing to help customers and provide prompt service.

|

|

4

|

Assurance

|

Knowledge and courtesy of employees and their ability of convey trust and confidence.

|

|

5

|

Empathy

|

Caring, individualized attention the firm provides its customers.

|

|

Source: Zeithmal, Parasuraman and Berry, (1988) Delivering

Quality Service, New York, Free Press, p 26.

|

Based on the five service quality dimensions, two sets of twenty-two statements

or questionnaire are developed, (Donnelly et al 1995 and Iwarden et al, 2003). The

questionnaires are a seven-point Likert scale. Robinson (1999) also explains that

one set is about customers expectations (expectation of service quality before using

the service) and the other set measures customer perceptions (perceptions of quality

after using the service). The difference between the two; perceptions (P) and expectations

(E) constitute the service quality gap. The quality gaps according to Parasuraman

(2004) and the Tahir and Bakar (2007) are five. These are:

- Gap 1: The difference between what customers really expect and what management think

(perceptions) of customers expectations. Donnelly et al (1995) are of the view that

the gap occurs because management did not undertake in-depth studies about customers’

needs. Also there are poor internal communication and insufficient management structures.

This gap is referred to as the understanding or knowledge gap.

- Gap 2: Is what is called standard gap. It is the difference between management perceptions

of customer service quality expectations and service quality specifications.

- Gap 3: This gap is also known as the delivery gap. The difference bewtween service

quality specifications and the actual service quality delivered. This means the

failure to ensure that service performance conforms to specifications. Donnelly

et al (1995) contend that the failure emanates from absence of commitment and motivation,

insuffient quality control systems and insufficient staff training.

- Gap 4: This is the communication gap. It arises because of the difference between

the delivery of service and the external communication regarding promises made to

customers. Examples of medium used for the external communication are media and

customer contracts, (Donnelly et al 1995).

- Gap 5: This gap is the difference between customers’ expectations of service

quality and the actual service received.

Service Quality Dimension in Banks

Several researchers have suggested that the search for universal conceptualization

of the service quality construct may be futile (Levist, 1981; Lovetock, 1983). The

service quality construct is either industry or context specific (Babakus and Boller,

1992). The measurement of the service quality construct is multidimensional. In

its original structure, service quality consists of five dimensions (Parasuraman

et al., 1988; Carman, 1990; Rust and Oliver, 1994). These are:

- The tangibility aspects of the service

- The reliability of the service provider

- The assurance provided by the service provider

- The responsiveness of the service provider; and

- The service provider’s empathy with customers

The included variables to measure the service quality of commercial banks were ranging

from seventeen to fifty seven variables (Narul Islam, 2005; Verma and Vehra, 2000;

Sharma and Mehta, 2004; Elango and Gudep, 2006; Sharma and Sharma, 2007; Bhat, 2004;

Levesque and Gorden, 1996; Bhat, 2005; Zillur, 2005; Gani and Bhat, 2003). In the

present study, the included service quality variables are twenty.

Review of Literature

It is relevant to refer briefly to the previous studies and research in the related

areas of the subject to find out and to fill up the research gaps. The following

are the some studies conducted by the eminent authors and practitioners on the area

of service quality of banks.

(Dhandabani, 2010), Examined the nature of linkage between service quality and customer

loyalty in Indian retail banking. Study used confirmatory factor analysis to identify

the service quality dimension. The resulted dimensions are Reliability, Responsiveness,

Knowledge and recovery; and Tangibles. The service quality dimensions lead to customer

satisfaction and the customers’ satisfaction leads to customer’s loyalty.

The structural equation model reveals that there is no significant direct linkage

between service quality and customers loyalty. At the same time, the service quality

has a significant indirect impact on customer’s loyalty especially through

customer’s satisfaction.

(Desta, 2011) Studied by assessing and measuring the banking service quality perception

of the SBI branch customers; and examining the relationship between service quality,

customer satisfaction and positive word of mouth and found that the expectations

of bank customers were not met and that the largest gap was found in the reliability

dimension. This dimension also had the largest influence on customer satisfaction

and overall satisfaction of bank customers had a positive effect on their word-of-mouth.

The study also suggested that input from employees on what constitutes “service

excellence” will be beneficial. The bank need to reassess “what customers

expect from the bank” and provide client specific services. It needs to invest

on employee training programs that will provide employees with an understanding

of service culture and service excellence particularly at front line levels. Employee

training programs should focus on interpersonal communication and customer care

factors in order to be able to meet the customers’ need for personalized service.

Study was conducted (Santhiyavalli, 2011) to evaluate the service quality of SBI

by adopting the SERVQUAL technique developed by A.parasuraman et al (1988) and found

that that among five dimensions ‘Reliability’, ‘Responsiveness’,

Empathy’ and ‘Tangibility’ are the major factors responsible for

customer satisfaction which stood at 90 percent regarding the services provided

by State Bank of India. Thus based on the percent level of customer satisfaction,

the State Bank of India has scope to improve the quality of the service rendered

to its customers to ensure their loyalty.

(Maya Basant Lohani, 2012) examined on service quality in selected banks and measured

in five dimensions by using SERVQUAL scale developed by Parasuraman et al (1988

and revealed that there exist a small perceptual difference regarding overall service

quality with the respective banks. The study of found that banks have more concentration

on the tangible factor like a computerization, physical facilities, etc. to attract

the customers. The dimensions Reliability, Responsiveness and Assurance are found

to be the most vital and strategic determinants of service quality and customer

satisfaction for both public and private sector banks. If banks want to sustain

customers on a long term basis, bankers should work towards 100% customer satisfaction

that automatically foster customer delight.

(Jain, 2012) In their study “Customer Perception on Service Quality in Banking

Sector: With Special Reference to Indian Private Banks in Moradabad Region”

try to learn and understand the customer perception regarding service quality and

to learn and understand the different dimension of service quality in banks. The

Sample size used is 100 and the sample universe is Moradabad. The service quality

model developed by Zeithamal, Parsuraman and Berry (1988) has been used in the present

study. The analysis reveals that among the private sector banks all the dimensions

of service quality are equally important.

(Dr. Rupa Rathee, 2014), Studied the service quality gaps in banks after nationalization

of commercial banks. With the entry of new generation, tech-savvy, private banks

the banking sector has become too competitive. Gap analysis was applied to find

the gaps between expected and performed service in private banks to find the difference

between male and female perception and expectation. This study provided an insight

into which attributes of service quality in private bank were most important in

providing satisfaction to customers and areas where significant gaps existed. It

concluded that the highest gap was found in the dimension of reliability and empathy

and suggested that the banks have to reduce this gap giving individual personal

attention to understand customer specific needs. The customers trust the public

sector banks. These banks have existed in the market for a longer period than the

private sector banks. The reliability factor is a positive factor for these banks.

Therefore private banks should position themselves in the market on the basis of

this dimension and promote themselves aggressively. It becomes imperative for the

private sector banks to train their employees to treat the customers with empathy.

Statement of Problem

Extensive research has been done by eminent scholars, academicians and practitioners

on service quality in the banking industry. All these studies have concentrated

on urban areas only. No concrete study found out the perceptions of rural customers

about the quality of banks’ services in India. There is a need for an extensive

study on the rural customers’ perceptions on the service quality in banking

service offered in rural areas. Hence this research study was undertaken.

Objectives of the Study

The following are the main objectives of the present paper:

- To measure and analyze the quality of services provided by Private Sector Banks

in rural areas of Karimngar district of Telangana State, India.

- To measure the customer satisfaction in selected private sector rural banks by analyzing

the gap between expected quality and their perceived quality of banking services

using SERVQUAL model.

Methodology

In this paper an attempt has been undertaken to carry out a descriptive study regarding

various factors of service quality in selected bank.

Data Collection

The study was conducted by taking HDFC bank branches in rural areas in Karimnagar

district of Telangana State. The required data was collected from two sources namely

Primary Data and Secondary Data. Primary data was collected through structured questionnaire

from the existing bank customers. Secondary data was collected from the previous

publications.

Sampling Unit

The sample unit consists of customers of the HDFC bank in Karimnagar district of

Telangana state in India. The respondents are farmers, Employees and Business Persons.

Size of the Sample1

|

Table - 4

|

|

SAMPLE SIZE

|

|

Particulars

|

No.

|

|

No. of Mandals Selected for the study (10% of the Total 57 Mandals in the District)

|

6

|

|

Target Groups (Farmers, Employees, and Business People)

|

3

|

|

No. of Respondents from each group

|

10

|

|

Total Sample Size

|

180

|

|

No. Respondents Responded

|

168

|

|

% of the Respondents Responded

|

93.33

|

Techniques of Analysis of Data

So, collected data was analyzed with the help of statistical tools such as averages,

percentages, paired sample test (PST) etc. The results are interpreted with the

help of percentages in a meaningful manner.

Data Analysis and Study Results

To collect the required data, two hundred and forty questionnaires were distributed

to selected six HDFC bank customers in rural areas to know their opinions on service

quality of bank in selected six mandals of Karimnagar district in Telangan state

in India and two hundred and twenty eight were returned. The response rate was 93.33

per cent. An average of 15.83 per cent of total respondents was responded from each

mandal.

- Demographical Analysis

|

Table – 5

|

|

Demographic Details of Respondents - HDFC Bank

|

|

Variable

|

Category

|

No.

|

Percentage (%)

|

|

Mandal Areas

|

Siricilla

|

20

|

12.35

|

|

Huzurabad

|

22

|

13.84

|

|

Jagitial

|

30

|

18.52

|

|

Jammikunta

|

30

|

18.52

|

|

Sultanabad

|

30

|

18.52

|

|

Metpally

|

30

|

18.52

|

|

Total

|

162

|

100.00

|

|

Gender

|

Male

|

159

|

98.15

|

|

Female

|

3

|

1.85

|

|

Total

|

162

|

100.00

|

|

Age

|

Less than 30

|

50

|

30.86

|

|

31 - 40

|

68

|

41.98

|

|

41 - 50

|

35

|

21.60

|

|

51 - 60

|

9

|

5.56

|

|

More than 60

|

0

|

0.00

|

|

Total

|

162

|

100.00

|

|

Marital Status

|

Married

|

148

|

91.36

|

|

single

|

14

|

8.64

|

|

Total

|

162

|

100.00

|

|

Educational Qualifications

|

Master Degree

|

18

|

11.11

|

|

Graduation

|

62

|

38.27

|

|

Professional Degree

|

10

|

6.17

|

|

Intermediate

|

29

|

17.90

|

|

SSC

|

33

|

20.37

|

|

Less Than SSC

|

10

|

6.18

|

|

Total

|

162

|

100.00

|

|

Occupation

|

Farmers

|

42

|

25.93

|

|

Business

|

60

|

37.04

|

|

Employees

|

60

|

37.04

|

|

SHGs

|

0

|

0.00

|

|

Total

|

162

|

100.00

|

|

|

|

|

|

|

Income

|

Less than Rs.50,000

|

2

|

1.23

|

|

Rs.50,001 - 1,00,000

|

37

|

22.84

|

|

Rs.1,00,001 - 5,00,000

|

98

|

60.49

|

|

Above Rs. 5,00,000

|

25

|

15.49

|

|

Total

|

162

|

100.00

|

The results of demographic profile of the respondents under study revealed that

gender was almost evenly split in the proportions of 98.15 per cent males and 1.85

per cent females. 30.86 per cent of the respondents were below the age group of

30 years. 41.98 per cent in between 31 – 40 years, 21.60 per cent of respondents

in between the age group of 41 – 50 years and 5.56 per cent in between the

age group of 51 – 60. 91.36 per cent of respondents were married and 8.64

per cent respondents were unmarried.

The highest number of respondents i.e. 38.27 per cent of the total respondents possessed

the degree qualification, 20.37 per cent had 10th class qualification,

17.90 per cent respondents had completed intermediate education, 11.11 per cent

possessed master degree qualification. The remaining 6.17 per cent of the total

respondents possessed professional qualification. 6.18 per cent of respondents had

possessed only formal education i.e. less than 10th class, these were

illiterates and mostly belonged to farmers.

The data relating to occupation shows that 37.04 per cent of the total respondents

belonged to business and employees category, 25.93 per cent belonged to farmer category.

The highest number respondents indicating 60.49 per cent of the total were in the

Rs. 1, 00,001 to Rs. 5, 00,000 income group. 22.84 per cent of the total 162 respondents

were fall in the income group of Rs. 50,001 – 1, 00,000 and 15.49 per cent

of total respondents were in the income group of Rs. 5, 00,000 above and remaining

1.23 per cent indicating only two respondents were in the income group of less than

Rs. 50,000.

EAVALUATION OF SERVICE QUALITY IN HDFC BANK IN KARIMNAGAR

|

Table – 6

ASSESSMENT OF SERVICE QUALITY IN HDFC BANK

|

|

Sl.

No.

|

Expected Quality (E)

|

Mean

|

Perceived Quality (P)

|

Mean

|

Gap

(E-P)

|

%

Gap

|

|

A. TANGIBLES

|

|

1

|

The Bank must possess the sophisticated and good looking infrastructure.

|

4.92

|

My Bank has the sophisticated and good looking infrastructure.

|

4.03

|

0.90

|

18.00

|

|

2

|

Physical facilities at banks should be visual and attractive.

|

4.90

|

Physical facilities at my banks are visual and attractive.

|

4.03

|

0.87

|

17.40

|

|

3

|

Bank employees have to be in neat dress and appear dignified.

|

4.90

|

My Bank employees are in neat dress and appearing dignified.

|

4.29

|

0.62

|

13.40

|

|

4

|

Materials (statements or passbook) with bank should be visual and excellent.

|

4.88

|

Materials (statements or passbook) with my bank are visual and excellent.

|

4.03

|

0.84

|

16.80

|

|

|

Total

|

19.60

|

Total

|

16.38

|

3.22

|

|

|

Average (19.60/4)

|

4.90

|

|

4.09

|

0.81

|

16.20

|

|

B. RELIABILTY

|

|

5

|

If the bank promises something, it will do.

|

4.87

|

If my bank promises something, it will certainly do.

|

3.91

|

0.96

|

19.20

|

|

6

|

If customers have problems, the bank has to show sincere interest in solving them.

|

4.88

|

If customers have problems, my bank will show sincere interest in solving it.

|

4.02

|

0.86

|

17.20

|

|

7

|

The bank ought to perform the services at right time.

|

4.90

|

My bank performs the services at right time. As per time mentioned.

|

4.00

|

0.91

|

18.20

|

|

8

|

The bank should provide service at the time it promises to do so.

|

4.88

|

My Bank provides service at the time it promises to do so.

|

3.95

|

0.93

|

18.60

|

|

9

|

The Bank should keep accurate/error-free records.

|

4.88

|

My Bank keeps accurate/error-free records.

|

4.25

|

0.63

|

12.60

|

|

|

Total

|

24.42

|

Total

|

20.13

|

4.29

|

|

|

Average (24.42/5)

|

4.88

|

|

4.03

|

0.86

|

17.20

|

|

C. RESPONSIVENESS

|

|

10

|

Employees of the bank ought to inform customers exactly when service will be performed.

|

4.87

|

Employees of my bank inform customers exactly when service will be performed.

|

3.61

|

1.26

|

25.20

|

|

11

|

The Bank employees ought to give excellent service to its customers

|

4.87

|

My Bank employees give excellent service to its customers

|

4.03

|

0.84

|

16.80

|

|

12

|

The Bank employees must be willing to help the customers.

|

4.87

|

My Bank employees are always willing to help customers.

|

4.02

|

0.85

|

17.00

|

|

13

|

The Bank employees should be always ready to respond to customers’ requests.

|

4.87

|

Bank employees always ready to respond to customers’ requests.

|

4.04

|

0.83

|

16.60

|

|

|

Total

|

19.60

|

Total

|

15.70

|

3.90

|

|

|

Average (19.60/4)

|

4.90

|

|

3.92

|

0.98

|

17.60

|

|

D. ASSURANCE

|

|

14

|

The Bank employees should always try to infuse confidence in the customers.

|

4.87

|

My Bank employees always try to instill confidence in customers.

|

4.02

|

0.85

|

17.00

|

|

15

|

Customers (you) have to feel safe in transactions with the Bank’s employees.

|

4.87

|

Customers (me) always feel safe in transactions with my bank’s employees.

|

4.15

|

0.72

|

14.40

|

|

16

|

The Bank employees always ought to be courteous and polite with customers.

|

4.87

|

My Bank employees always courteous and polite with customers.

|

4.13

|

0.74

|

14.80

|

|

17

|

The Bank must possess employees have complete knowledge to answer queries of customers.

|

4.87

|

My Bank employees have complete knowledge to answer queries of customers.

|

4.09

|

0.78

|

15.60

|

|

|

Total

|

19.60

|

Total

|

16.40

|

3.20

|

|

|

Average (19.60/4)

|

4.90

|

|

4.10

|

0.80

|

16.00

|

|

E. EMPATHY

|

|

18

|

The Bank has to give individual attention to customers.

|

4.87

|

My Bank gives individual attention to customers.

|

3.72

|

1.15

|

23.00

|

|

19

|

The Bank operating hours must be convenient to all customers.

|

4.87

|

My Bank operating hours is convenient to all the customers.

|

4.35

|

0.52

|

10.40

|

|

20

|

Bank employees ought to understand the specific needs of their customers.

|

4.87

|

Bank employees understand the specific needs of customers.

|

3.91

|

0.96

|

19.20

|

|

|

Total

|

14.70

|

Total

|

11.99

|

2.71

|

|

|

Average (14.70)

|

4.90

|

|

4.00

|

0.90

|

18.00

|

|

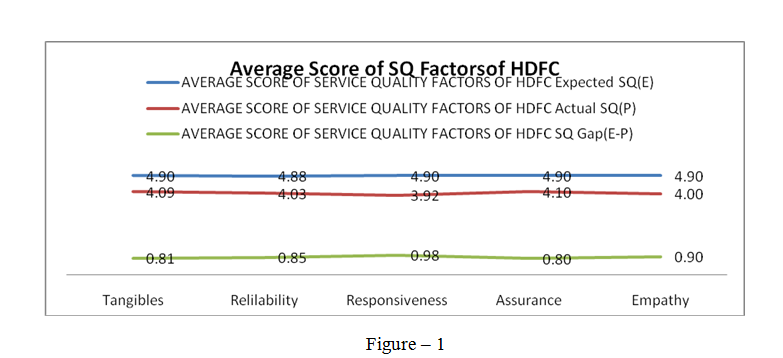

Table – 7

AVERAGE SCORE OF SERVICE QUALITY FACTORS OF HDFC

|

|

Sl. No.

|

Categories

|

Expected SQ (E)

|

Actual SQ (P)

|

SQ Gap (E-P)

|

per cent of Gap

|

|

|

1

|

2

|

3

|

4

|

(4*100)/5

|

|

1

|

Tangibles

|

4.90

|

4.09

|

0.81

|

16.20

|

|

2

|

Reliability

|

4.88

|

4.03

|

0.85

|

17.00

|

|

3

|

Responsiveness

|

4.90

|

3.92

|

0.98

|

19.60

|

|

4

|

Assurance

|

4.90

|

4.10

|

0.80

|

16.00

|

|

5

|

Empathy

|

4.90

|

4.00

|

0.90

|

18.00

|

|

|

Total

|

24.48

|

20.14

|

4.34

|

|

|

|

Average

|

4.90

|

4.03

|

0.87

|

17.40

|

The above tables 4.19 and 4.20 reveal that the level of expectation of the service

quality of the customers for dimentions namely tangibles, reliability, responsiveness,

assurance and empathy are rated between 4 and 5 points implies that the respondents

rated these dimentions in between ‘agree and strongly agree’. The level

of perceived quality regarding the above five dimentions rated by the respondents

between 3 – 5 implies ‘neutral to strongly agree for the services provided

by HDFC bank. The gap score is very less in ‘Assurance’ reveals that

customers are highly satisfied with the assurance aspects associated with the service.

Responsiveness and Empthy factors have the greater average gap score 0.98 and 0.90

respectively, implies dissatifaction of customers in respect to these factors.

|

Table – 8

Paired Samples Test

|

|

|

Paired Differences

|

t

|

df

|

Sig. (2-tailed)

|

|

Mean

|

Std. Deviation

|

Std. Error Mean

|

95per cent Confidence Interval of the Difference

|

|

Lower

|

Upper

|

|

TANGIBLES

|

|

Pair 1

|

EQ1 - PQ1

|

.500

|

.662

|

.052

|

.397

|

.603

|

9.617

|

161

|

.000

|

|

Pair 2

|

EQ2 - PQ2

|

.568

|

.609

|

.048

|

.473

|

.662

|

11.865

|

161

|

.000

|

|

Pair 3

|

EQ3 - PQ3

|

.309

|

.514

|

.040

|

.229

|

.388

|

7.640

|

161

|

.000

|

|

Pair 4

|

EQ4 - PQ4

|

.321

|

.693

|

.054

|

.213

|

.429

|

5.896

|

161

|

.000

|

|

RELIBILITY

|

|

Pair 1

|

EQ5 - PQ5

|

.586

|

.889

|

.070

|

.448

|

.724

|

8.394

|

161

|

.000

|

|

Pair 2

|

EQ6 - PQ6

|

.451

|

.740

|

.058

|

.336

|

.565

|

7.753

|

161

|

.000

|

|

Pair 3

|

EQ7 - PQ7

|

.352

|

.645

|

.051

|

.252

|

.452

|

6.945

|

161

|

.000

|

|

Pair 4

|

EQ8 - PQ8

|

.395

|

.653

|

.051

|

.294

|

.496

|

7.697

|

161

|

.000

|

|

Pair 5

|

EQ9 - PQ9

|

.296

|

.649

|

.051

|

.196

|

.397

|

5.812

|

161

|

.000

|

|

RESPONSIVENESS

|

|

Pair 1

|

EQ10 - PQ10

|

.512

|

.790

|

.062

|

.390

|

.635

|

8.255

|

161

|

.000

|

|

Pair 2

|

EQ11 - PQ11

|

.216

|

.507

|

.040

|

.137

|

.295

|

5.420

|

161

|

.000

|

|

Pair 3

|

EQ12 - PQ12

|

.222

|

.535

|

.042

|

.139

|

.305

|

5.292

|

161

|

.000

|

|

Pair 4

|

EQ13 - PQ13

|

.210

|

.551

|

.043

|

.124

|

.295

|

4.849

|

161

|

.000

|

|

ASSURNACE

|

|

Pair 1

|

EQ14 - PQ14

|

.259

|

.505

|

.040

|

.181

|

.338

|

6.530

|

161

|

.000

|

|

Pair 2

|

EQ15 - PQ15

|

.253

|

.477

|

.037

|

.179

|

.327

|

6.754

|

161

|

.000

|

|

Pair 3

|

EQ16 - PQ16

|

.191

|

.505

|

.040

|

.113

|

.270

|

4.822

|

161

|

.000

|

|

Pair 4

|

EQ17 - PQ17

|

.333

|

.610

|

.048

|

.239

|

.428

|

6.950

|

161

|

.000

|

|

|

|

|

|

|

|

|

|

|

|

|

EMPATHY

|

|

Pair 1

|

EQ18 - PQ18

|

.531

|

.973

|

.076

|

.380

|

.682

|

6.946

|

161

|

.000

|

|

Pair 2

|

EQ19 - PQ19

|

.426

|

.787

|

.062

|

.304

|

.548

|

6.892

|

161

|

.000

|

|

Pair 3

|

EQ20 - PQ20

|

.605

|

.783

|

.062

|

.483

|

.726

|

9.833

|

161

|

.000

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hypothesis

H0 = There is no significant difference between opinions

of customers of HDFC BANK Bank in

respect of expected and perceived quality.

HA = There is significant difference between opinions

of customers of HDFC BANK Bank in

respect of expected and perceived quality.

At the a = 0.05 level of significance, there exists enough evidence to conclude

that there is a difference between expected and perceived service quality variable

and dimensions that are ‘Tangibles”, ‘ Reliability’, Responsiveness’,

‘Assurance’ and ‘Empathy’. It is clearly establishes the

significant difference between expected and perceived service quality dimensions

of HDFC bank.

It is clear that there is difference in customers’ opinions of HDFC in respect

of the service quality. It requires the bank officials should more responsive and

respond immediately to the queries and provide the needed information to the customers.

Therefore it is needed proper attention of bank officials on adjusting the bank

operating timings that is convenient to all type of customers particularly employees

and make a focus on the needs of customers to reduce the service quality gap which

lead to increase the satisfaction level of customers.

Overall Service Quality of HDFC Bank

Having discussed the opinions of respondents from the selected HDFC bank in respect

of influencing factors, Importance and Actual quality of facilities and amenities,

service timings, service encounters and service quality aspects, an attempt is made

to study the opinions of respondents on overall service quality, SQ meeting the

needs of the customers overall satisfaction, loyalty and making recommendation to

relatives and friends. The analysis is presented in the following paragraphs.

Overall Service Quality of HDFC Bank

|

Table – 9

Overall Service Quality of HDFC Bank

|

|

Particulars

|

Frequency

|

Percent

|

Mean

|

SD

|

|

Very Poor

|

0

|

0

|

4.40

|

0.572

|

|

Poor

|

0

|

0

|

|

Average

|

7

|

4.3

|

|

Good

|

84

|

51.9

|

|

Very Good

|

71

|

43.8

|

|

Total

|

162

|

100.0

|

The table – 4.22 reveals that the opinions of the customers on overall service

quality of HDFC bank in Karimnagar district. The opinions are rated with the help

of 5 point Liker Scale’ ranging 1 – 5 points indiciating ‘Very

Poor – Very Good’. Repondents of HDFC bank rated the Overall Service

Quality between 4 – 5 implies ‘Good to Very Good’ for the services

provided by the bank. The highest number of respondents representing 51.90 per cent

of the total had expressed that the service quality of the bank as ‘good’

and following 43.80 per cent indicating 71 in number rated as ‘very good’.

Customer opined overall service quality as ‘average’ by 7 in number

representing 4.30 per cent. No customer rated the service quality as ‘poor

and very poor’.

It is tested to prove the relation between service quality (dependent variable)

and demographical details of respondents (independent variables) of HDFC bank through

paired sample t- test.

|

Table – 10

Paired Samples Test

|

|

|

Paired Differences

|

t

|

df

|

Sig.

(2-tailed)

|

|

Mean

|

Std. Deviation

|

Std. Error Mean

|

95per cent Confidence Interval of the Difference

|

|

Lower

|

Upper

|

|

Pair 1

|

Area of Bank - Overall SQ

|

-.667

|

1.858

|

.146

|

-.955

|

-.378

|

-4.566

|

161

|

.000

|

|

Pair 2

|

gender - Overall SQ

|

-3.377

|

.590

|

.046

|

-3.468

|

-3.285

|

-72.850

|

161

|

.000

|

|

Pair 3

|

Age - Overall SQ

|

-1.389

|

1.035

|

.081

|

-1.549

|

-1.228

|

-17.078

|

161

|

.000

|

|

Pair 4

|

Qualification - Overall SQ

|

-1.222

|

1.576

|

.124

|

-1.467

|

-.978

|

-9.869

|

161

|

.000

|

|

Pair 5

|

Occupation - Overall SQ

|

-2.284

|

1.006

|

.079

|

-2.440

|

-2.128

|

-28.897

|

161

|

.000

|

|

Pair 6

|

Annual Income - Overall SQ

|

-1.494

|

.858

|

.067

|

-1.627

|

-1.361

|

-22.163

|

161

|

.000

|

|

Pair 7

|

Marital Status - Overall SQ

|

-3.309

|

.653

|

.051

|

-3.410

|

-3.207

|

-64.530

|

161

|

.000

|

H0 – There is no significant relation between

service quality and bank type, area of the bank, age, gender, qualification, occupation,

annual income and marital status of the respondents of HDFC bank.

H1– There is significant relation between service

quality and bank type, area of the bank, age, gender, qualification, occupation,

annual income and marital status of the respondents of HDFC bank.

The significance value at 0.05 is zero, hence it is rejected the null hypothesis

and concluded that the difference in opinions of customers about service quality

due to bank type, area of the bank, age, gender, educational qualification, occupation,

annual income and marital status of respondents is significant and is just not a

matter of chance.

Overall Satisfaction against the Service Quality

After studying the responses of respondents of HDFC bank against various aspects

of service quality, an attempt is made to know their satisfaction level and furnished

in the table – 4.25. The opinions are rated with the help of 5 point Liker

Scale’ ranging 1 – 5 points indiciating ‘Very Dissatisfied –

Very Satisfied’.

|

Table – 11

Overall Satisfaction Against the Service Quality

|

|

Particulars

|

Frequency

|

Percent

|

Mean

|

SD

|

|

Strongly Dissatisfied

|

0

|

0

|

4.51

|

0.514

|

|

Dissatisfied

|

0

|

0

|

|

Neutral

|

1

|

.6

|

|

Satisfied

|

77

|

47.5

|

|

Very Satisfied

|

84

|

51.9

|

|

Total

|

162

|

100.0

|

The average of satisfaction level of repondents of HDFC Bank lied between 4 –

5 implies ‘satisfied to very satisfied’ for the services provided by

the bank. The highest number of respondents representing 51.90 per cent of the total

were very satisfied and following 47.50 per cent indicating 77 in number were satisfied.

Only one customer who was neutral either satisfied or dissatisfied in respect of

satisfaction level. No customer was dissatisfied with the services of HDFC bank.

|

Table 4.26

Paired Samples Test

|

|

|

Paired Differences

|

t

|

df

|

Sig.

(2-tailed)

|

|

Mean

|

Std. Deviation

|

Std. Error Mean

|

95per cent Confidence Interval of the Difference

|

|

Lower

|

Upper

|

|

Pair 1

|

Area of Bank - Overall Satisfaction

|

-.784

|

1.733

|

.136

|

-1.053

|

-.515

|

-5.758

|

161

|

.000

|

|

Pair 2

|

gender - Overall Satisfaction

|

-3.494

|

.549

|

.043

|

-3.579

|

-3.409

|

-81.027

|

161

|

.000

|

|

Pair 3

|

Age - Overall Satisfaction

|

-1.506

|

1.011

|

.079

|

-1.663

|

-1.349

|

-18.966

|

161

|

.000

|

|

Pair 4

|

Qualification - Overall Satisfaction

|

-1.340

|

1.631

|

.128

|

-1.593

|

-1.086

|

-10.453

|

161

|

.000

|

|

Pair 5

|

Occupation - Overall Satisfaction

|

-2.401

|

.929

|

.073

|

-2.545

|

-2.257

|

-32.902

|

161

|

.000

|

|

Pair 6

|

Annual Income - Overall Satisfaction

|

-1.611

|

.858

|

.067

|

-1.744

|

-1.478

|

-23.902

|

161

|

.000

|

|

Pair 7

|

Marital Status - Overall Satisfaction

|

-3.426

|

.588

|

.046

|

-3.517

|

-3.335

|

-74.194

|

161

|

.000

|

It is also tested to prove the relation between customers’ overall satisfaction

towards service quality (dependent variable) and demographical details of respondents

(independent variables) of HDFC bank through paired sample t- test.

H0 – Customers’ satisfaction does not vary

in respect of bank type, area of the bank, age, gender, qualification, occupation,

annual income and marital status of the respondents HDFC bank.

H1– Customers’ satisfaction varies in respect

of bank type, area of the bank, age, gender, qualification, occupation, annual income

and marital status of the respondents HDFC bank.

The significance value at 0.05 is zero, hence it is rejected the null hypothesis

and concluded that the difference in customers’ satisfaction towards service

quality due to bank type, area of the bank, age, gender, educational qualification,

occupation, annual income and marital status of respondents is significant and is

just not a matter of chance.

Conclusion

Service quality should be used as a strategic tool to get a competitive advantage

over the competitors. With the increasing levels of globalization of the Indian

banking industry, and adoption of universal banks, the competition in the banking

industry has intensified. Any where’ and ‘any time banking now become

a reality Recognition of service quality now acts as a competitive weapon.

The SERVQUAL model was used to assess and compare the service quality delivered

by three major banks operating in rural areas of Kaimnagar district. Analysis of

gap score reveals that the highest gap score in the dimension ‘Tangible’

(0.81) indicates poor service quality.

The results of the analysis show that the customers rated the bank rated in between

good and very good on all the five dimensions of service quality. In order to stay

competitive, the bank needs to improve on their service quality especially in the

identified areas ‘Tangibility’ and ‘Empathy’ which are the

major responsible factors for customer satisfaction regarding the services provided

by the bank. The Bank needs to be more responsive and train its staff how to show

empathy to their customers. The overall service quality obtained shows that, although

the customers are satisfied with the bank, still proper attention is require to

improve the service quality to retain the existing customers and to attract new

customers.

References:

Bhatia, M. B. (2012, October). Assessment of Service Quality in Public and Private

Sector Banks of India with Special Reference to Lucknow City. International Journal

of Scientific and Research Publications, 2(10), 1 - 7.

Bhatia, M. B. (n.d.). Assessment of Service Quality in Public and Private Sector

Banks of India with Special Reference to Lucknow City. International Journal of

Scientific and Research Publications,, 2(10), 1 - 7.

Desta, T. S. (2011, november). Perceived Quality of Services Rendered by Commercial

Banks: A Case Study of State Bank of. International Journal of Research in commerce

and Management, 2(11), 26 - 36.

Dhandabani, S. (2010, July-Dec.). LINKAGE BETWEEN SERVICE QUALITY AND CUSTOMERS

LOYALTY IN COMMERCIAL BANKS. International Journal of Management & Strategy,

1(1), 1-22.

Dr. Rupa Rathee, D. A. (2014, July). To Identify Service Quality Gaps in Banking

Sector: A Study of Private Banks. International Journal of Emerging Research in

Management &Technology, 3(7), 101-106.

Hung, Y. H. (2003). Service Quality Evaluation of Service Quality Performance Matrix.

Total Quality Management & Business Excellence, 14(1), 79 - 89.

Jain, V. G. (2012). "Customer Percepetion on Service Quality in Banking Sector".

With Special Reference to Indian Private Banks in Moradabad Region. International

Journal of Research in Finance & marketing (IJRFM), 2(2), 597-610.

Kotler, P. (2003). Marketing Management. NJ: Englewood Cliffs: Prentice-Hall.

Lewis, B. (1989). Quality in Service Sector - A Review. Interntional Journal of

Brand Marketing,, 7(5), 4 - 12.

Maya Basant Lohani, D. P. (2012, October). Assessment of Service Quality in Public

and Private Sector Banks of India with Special Reference to Lucknow City. International

Journal of Scientific and Research Publications, 2(10), 1 - 7.

Newmn, K. (2001). interrogting SERVQUAL: A Criticl Assessment of Service Quality

Measurement in a High Street Retail Bank. International Journal of Bank Marketing,

19(3), 126-139.

Santhiyavalli, D. M. (2011, September). Customer’s perception of service quality

of State Bank of India - A Factor Analysis. International Journal of Management

& Business Studies, 1(3), 78-84.

Wang. Y., H. &. (2003). The Antencedents of SErvice Quality and Product Quality

and their Influences on Bank Reputation: Evidence from Banking Industry in Chaina.

Managing Service Quality, 13(1), 72-83.

Wang.Y.Lo H & Huj, Y. (2003). The Antencedents of Service Quality and Product

Quality and Their Influence on Bank Reputation: Evidence from Banking Industry in

Chaina. Managing Service Quality , 72-83.