Investigating the relationship between characteristics of chief

executive officer and company ownership with investment cash flow sensitivity

|

Leila Shadman Panabandani

Department of Accounting

Rasht Branch

Islamic Azad University

Rasht, Iran

|

Mohamad Aghaei Bejarkenari

Department of Accounting

Rudbar Branch

Islamic Azad University

Rudbar, Iran

Email: Aghaei_m3@yahoo.com

|

Mehdi Meshki

Department of Accounting

Payame Noor University

Rasht, Iran

|

Abstract

The main purpose of the study is to investigate the relationship

between characteristics of chief executive officer and company ownership with investment

cash flow sensitivity. In order to assess the exact impact of each factor on

the dependent variables, each of these components were tested in the two main

hypotheses. The purpose of the study is applied and its method is descriptive-correlation.In

order to test the hypotheses, 74 companies of Tehran Stock Exchange from2010 to

2014 were selected from 370 companies. The results of the study showed a

significant negative relationship between the characteristics of chief

executive officer and company ownership with investment cash flow sensitivity.

According to the tests, there is a significant negative relationship between characteristics

of chief executive officer and company ownership with investment cash flow

sensitivity; that is, more optimistic chief executive officer and focus on

stock can result in the reduction of investment cash flow sensitivity.

Keywords: management optimism, investment cash flow sensitivity, company ownership

Introduction

An important purpose of financing is investing in companies to be

more profitable. To maximize the value of the company, company executives are

seeking to implement profitable investments; implementing these profitable

projects requires financing. The only source of funding is not shortage of bank

liquidity facilities and there are other solutions. Domestic financial

constraints are limitations in relation to resources (cash) within the business

unit and can be raised under the agency cost. The company reliance on domestic

resources can be determined through "investment cash flow

sensitivity" of that company. It is argued that companies that are

experiencing financial constraints possess more investment cash flow

sensitivity.To be able to finance their investment projects, companies that

suffer from more severe failure related to the capital market rely more on

domestic resources. Based on this idea, Fazzary et al. introduced an index

called "investment cash flow sensitivity" (Almedia, 2004). This index

is defined as measuring the rate of change in capital expenditure by companies

in exchange for a unit change in cash flow. Accordingly, the higher the sensitivity

of investment spending to corporate cash flows is, the more reliance the

company has on its domestic resources; therefore, it suffers from higher financial limitations. In addition, according to this

index, in the case of companies that suffer from serious capital market

imperfections, there is a higher sensitivity of investment cash flow

(Mohammadi, 2010).

To divide the company in terms of financing constraints, financial

constraints must be defined first. The most complete and most correct

definition in this case is thatwhen companies are faced with a gap between

internal and external costs of allocated funds, they are in the range of

financing.From among the main reasons for the differences between internal and

external financing costs, asymmetric information and agency problems can be

named. In the case of information asymmetry, investors have little information

about the status of companies' capital projects; therefore, in order to invest

in such companies, they demand a higher rate of return. Agency problems can

cause distrust between managers, and investors demand a higher rate of return

for financing the investment projects they charge.Based on the abovementioned

issues, it can be argued that companies suffering from serious failure related

to the capital market rely more on domestic sources in order to finance their

investment projects (Haqiqat, 2013).

Based on this idea, Fazzary et al. (1988) introduced an index

called "investment cash flow sensitivity." This index is defined as

measuring the rate of change in capital expenditure of company in exchange for

a unit change in cash flow. Accordingly, the higher the sensitivity of

investment spending to corporate cash flows is, the more reliance the company

has on its domestic resources; therefore, it suffers from higher financial limitations. In addition, according to this

index, in the case of companies that suffer from serious capital market

imperfections, there is a higher sensitivity of investment cash flow

(Mohammadi, 2013).

Managers have a critical role in organizational dynamics. They

provide the possibility of allowing flexibility and responsiveness to

environmental changes, pave the way for the coordination of different group

activities in the organization, satisfy individual needs, and facilitate

organizational membership. Philosophy of management is inextricably linked with

decision-making and,with a little thought, we find that managers donot do

anything except decision-making.In a sense, all actions of a manager are mixed

with decision. In addition to decision-making, managers have features and

characteristics that their crystallization in management distinguishes managers

from employees who are under their supervision. These characteristics and

features can be divided generally and specifically (Sadidi, 2014).

The first question that arises here thatwe are looking for an

answer to it in this study is whether there is a significant relationship

between the characteristics of chief executive officer and investment cash flow

sensitivity.

Organization for Economic Development (1998) defines corporate

governance as: "complex relationships between management (executive),

board of directors, shareholders and other relevant parties in a company."

In other words, corporate governance specifies a structure through which company

objectives are set, methods to achieve goals are determined, and, finally,

criteria and mechanisms of supervision and performance guidance are identified

(Asgari, 2014). Regardless of the legal framework, ownership structure of

companies can also affect the creation and development of the model of corporate

governance.Ownership structure has two dimensions: the ownership concentration

and identity of shareholders. Shareholders are the owners of the company who

assign business operations on behalf of themselves to managers that may result

in the conflict of interest. UK and America have a large number of Public Joint

Stock Companies which have widely dispersed ownership in most cases and

shareholders have little impact on the company's management, and they are

almost identical in terms of stock ownership structure;while in the countries

that are the origin and source of civil law, such as Japan and Germany, they

have concentrated ownership structure in most cases. Dispersed ownership structure

leads to faster agency problems. According to Solomon, separation of the role

of chief officer (chairman) and executive director is one of the ways to reduce

the agency problems. In addition, the study of Peel and Aodnel (1995) confirms

this issue and shows that, because of more independent managers' decisions,

companies that have such a breakdown, their financial performance has been

better. Thus, with the inclusion of recommendations on the roles of chief

officer and executive director by separate entities in the Combined Corporate

Governance Code, UK seeks to reduce agency problems. Similarly, Canada seeks to

strengthen shareholders'control on managers of the company by applying the same

procedures and breakdown of responsibilities at the head of the company. In

contrast, Daily and Dalton (1997) found no significant positive correlation

between company's performance and duty division of chief officers and executive

directors. Accordingly, the Sarbanes–Oxley Act considered the possibility of

running both roles as practical even though the ownership structure of

shareholders in America is highly fragmented.Because countries with civil law

have a weaker support of investors, ownership concentration is higher in these

countries; therefore, in a company with a relatively concentrated ownership

structure, conflict of interests is created between major shareholders and

minority shareholders. Conversely, in countries with common law, the rights of

investors are protected more effectively and, thus, ownership can be widely

distributed (Isfahan Portal). Now, the second question that can be raised here

is that "is there any significant relationship between company ownership

and investment cash flow sensitivity?"

Research methodology

The hardest step in any research process is to identify the problem

being studied. First, there should be an obstacle or an unclear doubt about one

thing, doubt that needs to be determined.In any study, the type, nature,

objectives, and its scope should be determined first so that it would be

possible to achieve reality by using proper rules and tools and finding valid methods.

Accordingly, this study is applied in terms of orientation and is descriptive in

terms of purpose. Applied research is a research the results of which can be

applied to meet needs and solve problems; therefore,the purpose of this type of

research is to apply it in solving specific problems in the community.

Descriptive research includes a set of methods aiming at describing the

conditions or phenomena under investigation. Conducting descriptive research

can help in the better understanding of current situation or the

decision-making process. Because this study used previous information in order

to explore the relationship between variables, it is classified as

causal-comparative research. In a causal-comparative research, data are

collected and analyzed from an environment that existed in a natural way or

from the past events that occurred without the interference of researcher's

system; thus, there is not the possibility of manipulating variables. In this

study, each of the data of the independent variables of the study was obtained

and then the dependent variable was obtained based on thequestionnaires from

thecollected samples.In the next stage, research hypotheses about the

relationship between each of the characteristics of the company's board of

directors and characteristics of the audit committee with the auditors' demands

for non-audit services was assessed using linear regression models.

Research Questions

This study raised the issue in a way that it can be explored

scientifically, and its measurement and testing will be possible, and it has

its scientific value. The points that are considered in this research are as

follows:

1.

Explaining the

main terms

2.

Expressing the

problem

3.

Expressing the

hypotheses

4.

The tools used

in the study

5.

The importance

of the research topic

Accordingly, the main research question is:

Is there any significant relationship between the characteristics

of chief executive officer and company ownership with investment cash flow

sensitivity?

Research hypotheses

Hypothesis is the researcher's solution to address the problem.

That's why developing a proper hypothesis depends on how the problem is

expressed and the roots of a suitable hypothesis are merged with expressing a

problem. Hypothesis is a hypothetical proposition which itsconfirmation or

rejection is tested based on concept consistency using empirical evidence and

knowledge of the past.

The importance of

a given hypothesis is judged in connection with its efficiency in the issue.

However, judgment about developed hypothesis requires the determination of the

criterion or criteria that evaluate features of a hypothesis.

According to the

abovementioned issued the following hypothesis can be raised:

1.

There is a

significant relationship between the characteristics of chief executive officer

and investment cash flow sensitivity.

2.

There is a significant

relationship between company ownership and investment cash flow sensitivity.

Research model

This study explores the sensitivity of changes in external

financing sources of the company in relation to changes in the cash flows under

financial constraints and the economic crisis in listed companies of Tehran

Stock Exchange. Accordingly, research hypotheses about the relationship between

each of the components of internal cash resources with sensitivity to financing

changes will be evaluated using linear regression. In order to test the first

and second hypothesis, the following formula was used (Ben Muhammad, et al.,

2014):

=investment

cash flow sensitivity

= constant value

=

regression coefficient

=company's growth opportunities

=net

cash flows from operating activities to total assets ratio

=management optimism

=ownership concentration

=company size

=company's financial leverage

=error term

Research

variables

The most

important and useful way to classify variables is dividing them into

independent and dependent variables. Because of the general applicability,

simplicity and importance in conceptualizing and planning as well as reporting

the results, this type of classificationis very useful.

Dependent

variable

Investment cash

flow sensitivity (I)

This index is

defined as measuring the rate of change in capital expenditures by companies in

exchange for a unit change in operating cash flow which is calculated as

follows:

Independent

variables

Independent variable is a variable

through which dependent variable can be predicted. This variable is measured,

manipulated or selected by the researcher so that its relationship with or its

effect on other variables can be measured.

Management

optimism

It is a dummy variable. If executive

directors have this condition, they receive number one; otherwise, they receive

zero number. To calculate it, the average net purchases of industrial materials

is calculated and, then, it is compared with the net purchases of the sample

manufacturing companies. If the net purchase of the company is higher than the

average, number 1 is attributed to it (manager is optimistic); if it is less

than the average, number zero is attributed to it (manager is not optimistic).

Ownership

concentration

It refers to share distribution among

shareholders of various companies. As the number of shareholders reduces, ownership

will be more concentrated. In this study, in order to calculate the ratio of

ownership concentration, the Herfindahl-Hirschman index (HHI) was used. This

index is obtained from the sum of squared percentage of shares owned by the

shareholders of the company. This index is increased in parallel with the

increased concentration of ownership, and in situations where the stock is

owned by one person, it allocates most of the value to itself and is calculated

equivalent to 10,000 units. If the ownership structure is dispersed and all

shareholders have equal ratios, HHI find the least valueand is calculated

equivalent to N/10,000. Herfindahl index can be calculated as follows

(Mohammadi, Qalibaf Asl, & Meshki, 2010).

Control variable

Company's growth opportunity (QTobin)

This

proportion is used as a measure of value. The mentioned ratio can be calculated

by dividing the market value of assets into their final replaced cost which can

be calculated as follows:

=the

market value of equity

=book

value of debts

=. book value of assets

Net cash flows from operating activities to total assets ratio (CF)

Company size

Company size is calculated through natural logarithm of total

assets as follows:

Company's

financial leverage

It is obtained

by dividing total debt (TL) into total asset (TA) of the company which formula

is as follows:

To determine

the specific sample in this study, companies that their data was available were

used. The statistical sample was selected from the companies listed in Tehran

Stock Exchange which had all the following conditions:

1.

Companies that

had activities in Tehran Stock Exchange and the data related to them were

available from2010 to 2014.

2.

Companies that

their stock had been traded in the exchange from 2010 to 2014 and their symbolwill

have not been removed from the exchange board by the end of the fiscal year of 2014.

3.

The fiscal year

ended on March of each year.

4.

Companies do

not lose money in these years.

5.

Companies that their

symbol had not a trading delay more than 6 month.

6.

The companies

should not be banks, financial institutions, insurance companies, holding,

investors, andthe like.

7.

The companies

should be manufacturing.

According to

the abovementioned terms, 74 companies listed on the Tehran Stock Exchange,

whose information was disclosed, were selected and their financial statements were

examined. Therefore, according to table (1), 74 companies were selected as

sample.

Table 1.

The number of companies being studied

|

Number

|

Explanation

|

|

317

|

The initial number

|

|

- 58

|

Investment

and holding companies

|

|

- 66

|

The

companies that are not leading up to 29/12

|

|

- 48

|

Companies

that lose money

|

|

- 13

|

Companies

that their data was not available

|

|

- 58

|

Companies

that did not purchase raw materials

|

|

74

|

Companies being studies

|

Data analysis

The first step

in any statistical and data analysis is the calculation of descriptive indices.

Therefore, in order to start data analysis, descriptive statistics of data

including central tendency, dispersion and deviations from symmetry and also Jarque

and Bera test checks for normally distributed residuals were calculated, and

the results are shown in the following table.

Table

2. Introduction and separation of the symbols used for the variables of the

model

|

Row

|

Variable symbol

|

Variable name

|

Variable type

|

|

1

|

I

|

Investment cash flow sensitivity

|

Dependent

|

|

2

|

OPTIMISM

|

Management optimism

|

Independent

|

|

3

|

OWNER

|

Ownership concentration

|

Independent

|

|

4

|

CF

|

The ratio

of net cash flows

|

Control

|

|

5

|

QTobin

|

Company's

growth opportunity

|

Control

|

|

6

|

SIZE

|

Company size

|

Control

|

|

7

|

LEV

|

Company's financial leverage

|

Control

|

Table 3.

Descriptive statistics of variables before normalization

|

LEV

|

SIZE

|

OWNER

|

OPTIMISM

|

CF

|

QTobin

|

I

|

|

|

0/59

|

6/025

|

4080/897

|

0/5

|

0/1354

|

1/841

|

7/2

|

Mean

|

|

0/603

|

5/964

|

3782

|

0/5

|

0/114

|

1/576

|

0/051

|

Median

|

|

1/009

|

7/817

|

9218

|

1

|

0/558

|

15/851

|

2470/07

|

Maximum

|

|

0/048

|

4/441

|

1246

|

0

|

-0/298

|

0/864

|

-

25/618

|

Minimum

|

|

0/16

|

0/533

|

1817/071

|

0/5

|

0/129

|

1/104

|

128/53

|

Standard deviation

|

|

-0/41

|

0/544

|

1/0646

|

0

|

0/496

|

6/484

|

19/094

|

Skewness

|

|

3/159

|

4/144

|

3/812

|

1

|

3/371

|

73/929

|

366/653

|

Elongation

|

|

10/741

|

38/409

|

80/066

|

61/667

|

23/397

|

80151/94

|

2057871

|

Jarque-Bera

|

|

0/005

|

0/000

|

0/000

|

0/000

|

0/000

|

0/000

|

0/000

|

The statistics probability

|

|

370

|

370

|

370

|

370

|

370

|

370

|

370

|

Total data

|

|

74

|

74

|

74

|

74

|

74

|

74

|

74

|

Section

|

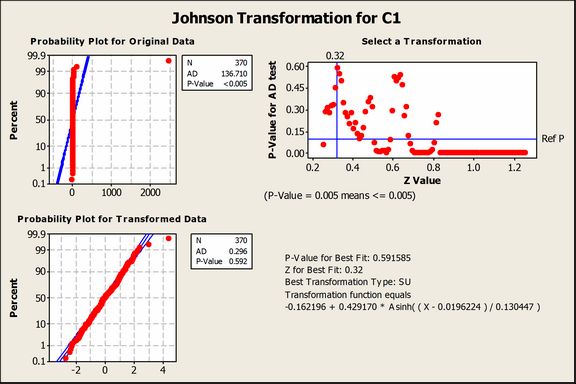

Given that the probability of Jarque-Bera statistics for the

dependent variable is less than 5%, H0 hypothesis is rejected

based on the normality of the error term and the dependent variable. To

normalize, Johnson transformation in the MINITAB software was used; the dependent

variable transfer function is provided in the diagram (1).

Diagram 1. Johnson transformation

normality test for the dependent variable I

As can be seen in the diagram (1), the dependent variable of the

study was not normal at first. After doing Johnson transformation, the

dependent variable became normal. In an abnormal mode, the probability of Jarque-Bera statistics was not at the significant level of

95% (p-value<0.05 ( , but, after

doing Johnson transformation test, the probability

of this statistics was at the significant level of 95% (p-value<0.05 ( .

The results of carried out tests

In this section of the study, after entering data into the software

and initial estimates of parameters, the presence or absence of a separate y-intercept

for each of the companies should be examined. At first, F-Limer test should be

examined and chosen between fixed or random effects in which H0

hypothesis, the same y-intercept (Pool), is in contrast with H1

hypothesis, inconsistency of y-intercept (Panel).In the Eviews 8 software, after testing the effect of fixed effects, if the

probability of the output statistics of the software is less than 0/05, the

panel method is accepted at the level higher than 95 percent; but if it is

greater than 0/05, the pooled method is accepted.

Chow test or structural changes test related to the hypotheses

(F-Limer)

Table 4. Chow test output

|

Test Summary

|

Statistics

|

Degrees of freedom

|

The statistics probability

|

|

Section F

|

2/561 |

73,290 |

0/000

|

As can be seen, the statistics probability is less than 0/05.

Therefore, regression has a different y-intercept; that is, y-intercepts are

not alike. Thus, model is accepted with the panel data.

Hausman test

H0 = There is no

correlation between individual effects and explanatory variables Random effects model

H1 = There is a

correlation between individual effects and explanatory variables Fixed effects model

Table 5. Results of Hausman

test

|

Test Summary

|

Statistics

|

Degrees of freedom

|

The statistics probability

|

|

Hausman

|

9/617

|

6

|

0/0474

|

As it is evident in the above table,

regarding the significant level which is less than 0/05, H1

hypothesis is accepted and the fixed effects model is selected as the preferred

model for research hypotheses at this stage.

Hypothesis testing

1.

There is a significant relationship between the characteristics of

the chief executive officer and investment cash flow sensitivity.

2.

There is a significant relationship between company ownership and

investment cash flow sensitivity.

Table 6.

The results of estimating the model of the first main hypothesis

|

Statistics

probability

|

t

statistics

|

Standard

deviation

|

coefficient

|

Variable

name

|

|

0/9133

|

0/109

|

0/26

|

0/028

|

C

|

|

0/0029

|

3/0169

|

0/01

|

0/027

|

Q

|

|

0/000

|

7/044

|

0/131

|

0/921

|

CF

|

|

0/0042

|

2/895

|

0/099

|

- 0/288

|

OPTIMISM

|

|

0/0465

|

- 2/002

|

-5/68

|

- 0/001

|

Owner

|

|

0/0027

|

3/029

|

0/241

|

0/730

|

Lev

|

|

0/000

|

-9/029

|

0/04

|

- 0/358

|

AR (1)

|

|

5/308

|

F statistics

|

0/536

|

Adjusted

|

|

2/41

|

Durbin Watson

|

0/000

|

F significant level

|

As can be seen in the above table, considering F

statistics, it can be said that the above regression model is significant. And

the Durbin-Watson statistic is equal to 2,41 after the arrival of the

self-return at the first time and the value of this statistic becomes suitable

and showed no correlation between model components. The adjusted coefficient of

determination of the model indicates that the model variables have the

explanatory power (54 percent) in order to explain the dependent variable.

According to the probability statistics of management optimism (OPTIMISM) that

is less than 0.05, it can be said that there is a significant negative

relationship between the characteristics of the chief executive officer and

investment cash flow sensitivity with a 95% margin of error, and hypothesis H0

is accepted. Moreover, considering the probability statistics of ownership

concentration that is less than 0.05, it can be stated that there is a

significant negative relationship between company ownership and investment cash

flow sensitivity with a 95% margin of error, and hypothesis H0

is accepted.

Summary and conclusion

In this

section, the results of testing the research hypotheses are generally reflected

in the following table.

Table 7. Summary of the general results of the

study

|

Hypothesis

|

Research hypotheses

|

Results

|

|

1

|

There is a

significant relationship between the characteristics of the chief executive

officer and investment cash flow sensitivity

|

Accepted

|

|

2

|

There is a

significant relationship between company ownership and investment cash flow

sensitivity.

|

Accepted

|

Reviewing and

comparing the results with previous research

Testing the

first research hypothesis showed a significant negative relationship between

the characteristics of the chief executive officer and investment cash flow

sensitivity. In addition, testing the second hypothesis indicated a significant

negative relationship between company ownership and investment cash flow sensitivity;

that is, as management optimism and ownership concentration decrease,

investment cash flow sensitivity increase. The findings of the study are

consistent with the findings of Ben Muhammad et al. (2014) who believe that

management bias can explain investment policies in large companies and can

change the cash.

Research limitations

According to

the terms of variables, the possibility of doing research on all companies was

not possible and so this issue tends to reduce the number of the samples, and

generalizing the results to other enterprises should be done with cautious.

Suggestion based on research results

Since managers tend to indulge in the use of internal funds, they

act with greater sensitivity regarding investment decisions and capital expenditures.

For example, it is better to invest more in the purchase of raw and related

production materials. In addition, because ownership concentration or stock

distribution has a significant effect on the investment sensitivity, it is

better that stock be distributed among fewer individuals.

Table 8.

Descriptive statistics of the variables after normalizing

|

LEV

|

SIZE

|

OWNER

|

OPTIMISM

|

CF

|

QTobin

|

I

|

|

|

0/59

|

6/025

|

4080/897

|

0/5

|

0/1354

|

1/841

|

-0/013

|

Mean

|

|

0/603

|

5/964

|

3782

|

0/5

|

0/114

|

1/576

|

-0/061

|

Median

|

|

1/009

|

7/817

|

9218

|

1

|

0/558

|

15/851

|

4/362

|

Maximum

|

|

0/048

|

4/441

|

1246

|

0

|

-0/298

|

0/864

|

-2/726

|

Minimum

|

|

0/16

|

0/533

|

1817/071

|

0/5

|

0/129

|

1/104

|

1

|

Standard deviation

|

|

-0/41

|

0/544

|

1/0646

|

0

|

0/496

|

6/484

|

0/179

|

Skewness

|

|

3/159

|

4/144

|

3/812

|

1

|

3/371

|

73/929

|

3/484

|

Elongation

|

|

10/741

|

38/409

|

80/066

|

61/667

|

23/397

|

80151/94

|

5/598

|

Jarque-Bera

|

|

0/005

|

0/000

|

0/000

|

0/000

|

0/000

|

0/000

|

0/061

|

The statistics probability

|

|

370

|

370

|

370

|

370

|

370

|

370

|

370

|

Total data

|

|

74

|

74

|

74

|

74

|

74

|

74

|

74

|

Section

|

Suggestions for future

The nature of scientific research is continuous and diverse. Perhaps

this sentence that in order to reach results, there are thousands of untested

methods in scientific approach is not far from reality. Therefore, based on

this reality, the following suggestions are presented below:

ü It is suggested that this type of research be conducted in various

industries and then the results be compared in these industries.

ü Regarding the importance of investment sensitivity and its effect

on the operating cash flow, it seems that further studies could reveal new

dimensions of the matter and boost literature in this area. Research on

different aspects of this subject is suggested to future researchers.

ü Using other methods to calculate the variables of the study, such

as the independent variable of management optimism using the interest

prediction rate per share and the independent variable of ownership

concentration using Tower index, is suggested.

ü There are various methods to calculate the index of ownership

concentration, such as total stock of real and legal entities who hold more

than 10% of shares (Tower, 2006), but this study used the Herfindahl-Hirschman

index.

ü To calculate the size variable, the natural logarithm of market

capitalization can be used, but, in this study, with the assumption of

reevaluation in the companies being studied, the natural logarithm of the book

value of assets was used based on Base article.

References

Almeida, H., Campello, M., Weisbach M.S., 2004. The cash flow

sensitivity of cash. Journal of Financial . No 59,1777– 1804

Asgar, A. A. (2014). Exploring the relationship between

investment structure with ownership structure and corporate diversification.

Master's thesis, Azad University of Rasht.

Fazzary, s, hubbard, R,G,& Petersen, B.(1988).Financing

constraints and corporate investment.

Haqiqat, H. & Zargar Fayuji, Y.

(2013). The impact of financial constraints and held cash on the sensitivity

of investment to cash flow. Applied research on financial reporting, 2nd

year, No. 3. Autumn and winter 2014.

Mohammadi, Sh., Ghalibaf Asl, H.,

& Meshki, M. (2010). Exploring the effect of ownership structure

(concentration and composition) on the performance and value of companies

listed on the Tehran Stock Exchange. Financial research, Vol. 11, Issue 28,

pp. 69-88.

Sadidi, M. & Mohammadi, A.

(2014). On the relationship between investment cash flow sensitivity with

the level of investment spending. Experimental Studies Quarterly of

Financial Accounting, eleventh year, spring, No. 41.