A Refereed Monthly International Journal of Management

IMPACT OF MULTI FIBRE AGREEMENT (MFA) PHASE OUT ON INDIAN TEXTILE EXPORTS

|

Greeshma Manoj

Assistant Professor

Dept of Economics

Christ University, Bangalore, Karnataka, India- 560029

Contact No.- +91 7259529756

Email: greeshma.manoj@christuniversity.in

|

S.Muraleedharan

Associate Professor (Retd)

Dept of Economics

Maharajas College, Cochin, Kerala, India.

|

Abstract

The Multi Fibre Agreement (MFA) and the system of bilateral quotas that had governed

the global trade in textiles and apparel for the past forty years came to an end

and were replaced by the Agreement on Textiles and Clothing (ATC) on Jan 1, 2005.

The dismantling of quota restrictions had brought about a significant change in

the structure of worldwide trade in textiles as there are no quota barriers for

the export of textiles and apparels and the hitherto protected textile industry

would be exposed to international competition. The withdrawal of the MFA had brought

back the comparative advantages of developing economies to large labour surplus

economies such as China and India. Since India has a natural comparative advantage

in cotton and cotton-based fibres, abolition of the MFA had an implicit potential

to benefit India's cotton industry as well as cotton based textiles and clothing

sectors. Compared to the competitors India enjoys certain advantage in the production

of textiles and clothing. At the same time, Indian textile industry is also facing

many challenges in the domestic and export front in the changed scenario. In the

given context, the present study attempts to analyse the export performance of Indian

textiles in the post quota era. Export performance has been analysed in terms of

change in the composition and destination of Indian textile exports in the post

MFA period. The period of study is from 1990-2012. In order to examine the impact

of quota removal (MFA), the study period have been sub-divided into Pre-MFA (1990-2004)

and post MFA (2005-2012) The study is based on secondary data drawn from Ministry

of Textiles, RBI and WTO. The study found that Compound Annual Growth Rate (CAGR)

of Indian textile exports were low during the post MFA period compared to pre MFA.

If we compare the average export value during the study period, it can be seen that

the mean value of textile exports are higher during the post MFA compared to pre

MFA period. Among the different sub sectors highest mean value was recorded in readymade

garments followed by cotton textiles and manmade textiles during the post MFA period.

Analysis of percentage share of different subsectors during the study period show

that readymade garments still constitute the largest share in terms of overall textile

exports followed by cotton textiles and manmade textiles. As far as the destination

of exports are concerned, USA could maintain its position as the largest destination

for Indian textile exports in the segment of textiles, readymade garments, coir

and carpets even during the post MFA period. Emergence of UAE as the single largest

destination for cotton textile exports in the post MFA period is noteworthy. It

can also be seen the emergence of new trading partners like Turkey (jute textiles

and manmade textiles), Egypt (cotton textiles) and UAE (cotton textiles and readymade

garments) in the post MFA period.

Key Words: MFA, textiles, quota restrictions, exports and compound annual

growth rate.

INTRODUCTION

India’s textiles sector holds a significant role in Indian economy as it is one

among the earliest established industries and the growth and development of this

sector has a direct bearing on the economic development of India. It is one of the

prominent sectors of Indian economy in terms of its contribution to output, employment

and foreign exchange earnings. It is the second largest employment provider, after

agricultural sector. Currently, it contributes about 14 percent to industrial production,

4 percent to the GDP, and 17 percent to the country’s export earnings. The structure

of Indian textile industry is unique and complex. Indian textile industry is characterised

by the predominance of organised sector which contributes to around 97 percent of

total cloth production and the share of unorganised sector is only 3 percent (Annual

Report 2014-15, Ministry of Textiles).

Textiles and clothing is a very important sector of international trade that has

served as the engine of growth, particularly for developing and least developed

countries. India is the second largest producer of textiles and garments in the

world next to China. The Indian textile industry has significant presence in the

world textile economy by virtue of its contribution to world textile capacity and

production of textile fibres/yarns. The Indian textile industry accounts for about

24 percent of world’s spindle capacity and eight percent of global rotor capacity.

At the global level, India’s textile exports account for just 4.72 percent of global

textile and clothing exports. The export basket includes a wide range of items including

cotton yarn and fabrics, man-made yarn and fabrics, wool and silk fabrics, made-ups

and a variety of garments. The Indian textile industry is currently estimated around

US $ 108 billion (CCI Report, 2015).

The international trade in textiles and clothing were governed by various trade

restrictions. Multi Fibre Agreement (MFA) was an important quantitative trade restriction

imposed by the developed countries to restrict the textile exports from developing

countries. The Multi Fibre Arrangement grew out of a series of s voluntary export

restraints imposed by the United States and Europe on large Asian textile and clothing

exporters (Spinanger, 1999). The first of such agreement was in the form of a Short

Term Arrangement Regarding International Trade in Cotton Textiles (STA) in 1961under

the General Agreement on Tariffs and Trade (GATT) followed by Long Term Agreement

Regarding International Trade in Cotton Textiles (LTA) in February 1962 which was

negotiated among 22 major trading nations to allow importing nations to use quotas

to avoid market disruption [1]. The multi fibre arrangement was later negotiated

in 1974 to broaden the scope of regulation as well as to provide a framework of

rules and procedures under which countries can impose import restrictions. The MFA

was a general, multilateral framework for managing textile and clothing trade for

cotton, wool and manmade fibres. MFA quotas were applied on a discriminatory basis

to some exporting countries but not to others, thus differing from country to country

in both product coverage and the degree of restrictiveness. It is designed to restrict

low-cost exports of clothing and textiles to developed-country markets. At the same

time, MFA was not applicable to trade between the rich developed countries and to

exports from the Least Developed Countries. The MFA resulted in restricting the

size of the textile industry in the exporting countries with natural competitive

advantage in the area, as no country could export more than the quota allocated

to it. In 1995, MFA was integrated into GATT via the Agreement on Textiles and Clothing

(ATC).

ATC was a transitory regime between the MFA and the integration of trading in textiles

and clothing in the multilateral trading system. The ATC envisaged the dismantling

of the Multi Fibre Agreement over 10 year period (1995-2004). The ATC provided for

(a) progressive elimination of quotas in selected products in four stages during

the transitional period ending in 2005 (b) increase in quota growth rates on remaining

products at subsequent stages.

Table 1: Schedule of Quota Integration under ATC

|

Stage

|

Date

|

Percentage of product to be brought under removal of quotas

|

|

I

|

1 Jan, 1995

|

16

|

|

II

|

1 Jan, 1998

|

17

|

|

III

|

1 Jan, 2002

|

18

|

|

IV

|

1 Jan, 2005

|

49

|

Source: WTO

With the termination of the Agreement on Textiles and Clothing (ATC) at the end

of December 2004, all textiles and clothing products were fully subject to multilateral

disciplines under the rules of the World Trade Organization (WTO). The elimination

of MFA quotas under ATC was expected to create a new environment for world trade

in textiles and apparel by vastly increasing the scope for developing countries

to expand their exports and thereby creating employment in this sector. Although

ATC has removed the quota restrictions on textile trade there was no consensus among

the policy makers with regard to the impact of quota removal on developing countries.

Within the developing countries there are quite large differences in competitiveness.

One of the major perceptions about the removal of quotas was that after the removal

India would become a major beneficiary because of the advantage of large manufacturing

base and a large supply of relatively low cost skilled workers. The scrapping of

MFA has raised many discussions about the new international trade climate. The elimination

of quotas was regarded as an opportunity as well as a threat for the competing countries.

Opportunity in the sense that the market is no longer restricted by quotas and threat

because competition became severe after the quota removal. India had great hopes

of achieving a rapid growth in textiles and clothing exports as quotas disappeared.

The general perception was that countries that take the opportunity to streamline

their policies, and improve their competitiveness would gain from the quota abolition.

REVIEW OF LITERATURE

There are a plethora of studies which have tried to analyse the impact of removal

of quota restrictions on the trading partners. However, they disagree on the impact

of quota elimination on developing countries. Most of the review studies done by

international organizations such as the WTO, the World Bank, the Asian Development

Bank and the United Nations, concluded that there would be enormous gains for both

developed and developing countries such as India after the removal of quota restrictions.

But there are some studies such as Spinanger (1998) and Martin and Winters (1996)

which hold much more cautious views, particularly with regard to developing countries,

on this scenario after 2005. Their assertion is that developing countries would

experience negative results after the elimination of textile quota restrictions.

Here the cited reviews are the ones which have analyzed the implications with reference

to Indian context.

Mehta. R (1997) found that the removal of MFA has provided opportunities and challenges

to India's exports of textile and clothing sector. The results show that the removal

of MFA has been advantageous to India's exports. India's export of textile and apparel

has significantly improved in the post-MFA regime. This increase has been due to

(i) increased import demand, and (ii) trade diversion of 'other countries' in destination

(developed) countries. Further, the increase has not been restricted to a few commodities,

but almost all commodities.

(Chadha and Pohit, 1999) analysed the potential gains from abolition of MFA for

developing countries, particularly India by using a 23 sector multi country Computable

General Equilibrium (CGE) NCAER-UM model of World Trade, Production and Employment.

Maximum welfare increase is observed in South Asia other than India. The analysis

also showed ASN region as the major gainer, in percentage terms, in the output of

textiles (14.5 percent) followed by NIE (8.5 percent), RSA (7.5 percent) and IND

(5 percent). India turns out to be a major proportional gainer in exports of both

textiles as well as clothing sectors (26 percent and 42 percent) followed by ASN

(19.5 percent), RSA (17 percent) and NIE (8 percent).

Nanda and Raikhy (2000) observes that in order to improve the market share in the

post MFA regime there is an urgent need to diversify into a high range and classic

garments, technology up gradation through imports importation, if necessary; up

gradation of labour skill, extension of off-shore production facilities to selected

clothing, in special areas like Andaman Nicobar etc.

Vijaya Ramachandran (2001) in her study identified the weak links in the production

chain, key obstacles to productivity and to exports, and policy changes that must

be made for the growth of production and exports in the textiles and garments sector

in the post MFA regime. The study identified three key weaknesses in the production

chain -the inability of Indian producers to supply an adequate amount of cloth,

particularly manmade; the lack of availability of textile machinery; and the lack

of downstream capacity in weaving and processing.

Kathuria, Martin and Bharadwaj (2001) evaluate the possible implications of MFA

removal on exports of garments and textiles focusing on India and the study showed

the discriminatory character of MFA. While the abolition of quotas on international

trade in textiles in 2005 will create opportunities in 2005 will create opportunities

for developing countries, it will also expose them to additional competition from

other formerly restrained exporters. The outcome for any country will depend on

its policy response. Countries that take the opportunity to streamline their policies

and improve their competitiveness are likely to gain from quota abolition.

Verma (2002) analyzed the competitive performance of Indian exports in US and EU

markets. It was found that except made ups, Indian textile export to the US had

no future. The market share of other products was declining. In case of EU, India’s

performance was good in synthetic products (yarn and made-ups) in textiles. Among

garments; suits, coats, jackets and skirts were leaders. The products whose exports

to EU had been constrained by quotas and hence were likely to gain from quota dismantling

in 2005 were cotton bleached fabric and woven bed linen.

Exim Bank (2005) estimated that in the short term, both China and India would gain

additional market share proportionate to their current market share. Exim Bank estimated

that India would have a market share of 13.5 percent in textiles and 8 per cent

in garments in USA market. With regard to EU, it was estimated that the benefits

were mainly in the garments sector. The potential gain in textile sector was limited

in the EU market considering the proposed further enlargement of EU. It was estimated

that India would have a market share of 8 percent in EU textiles market as against

China‘s market share of 12 percent.

Landes et al. (2005) opined that demand for cotton and manmade fibers in India would

likely to strengthen in response to rising consumer demand in India and increased

exports of textiles and apparel following the removing of the MFA quotas. The pace

of growth in cotton demand would hinge on execution of reforms to policies, including

taxes that discriminate against the use of manmade fibers and regulations affecting

the scale, technology use and export competitiveness of the textile and apparel

industries.

Ananthakrishnan and Chandra (2005) analyse the impact of the quota elimination on

India using Global Trade Analysis Project (GTAP -6) in two scenarios. Scenario I

assume a full elimination of quotas, while scenario II assumes a partial elimination

of quotas for China and a full elimination for other countries. The results of the

simulations do not present an optimistic scenario for India in terms of export growth

of Textiles and Clothing in quota free world (Scenario I). They also show that Indian

exports of textiles and clothing will continue to expand in the presence of the

safeguards on China, but will be adversely affected once these are lifted (Scenario

II).

Singh and Kundu (2005) analyzed competitiveness of Indian cotton textile industry

in the wake of liberalization. The study was conducted through an empirical investigation

of 81 senior and middle level executives from cotton textiles manufacturing and

exporting firms in India. The study found that even though globalization had opened

vast market opportunities for Indian cotton textile industry, the industry was exposed

to the threats of fierce competition. The study found that China, Vietnam, Bangladesh

and Malaysia were emerging as major competitors in international textile market.

It was also found that the industry was competitive in terms of input factors –

labour, transportation and raw material but not in terms of finance, power and technology.

From the above reviews, it has been clear that there is no consensus among the researchers

regarding the effect of quota phase out on Indian textile exports. Some of the studies

have portrayed a beneficial result to India in the post quota scenario while there

are studies which depict a gloomy picture for Indian textile exports in the post

MFA period. In the given context, the focus of the present study is to understand

the impact of quota removal on the exports of Indian textile exports in the post

MFA period after 2005.

DATA AND MEASURES

The analysis of export performance has been done with the help of secondary data

collected from published sources. Export data has been collected mainly from Handbook

of Statistics on Indian Economy from RBI as well as CMIE data base. The period of

study covers 22 years (1990-2012). In order to examine the impact of quota removal

(MFA), the study period have been sub-divided into Pre-MFA (1990-2004) and Post

MFA (2005-2013). In the Pre MFA period, there are 4 Phases: I phase (1995-96 to

1997-98), II Phase (1998-89 to 2001-02) and III Phase (2002-03 to -2004-05) and

IV phase (2005-2012). The export data in current prices has been converted into

constant prices by using the WPI deflator to remove impact of price fluctuation.

Export data for different subsectors have been deflated with the corresponding price

deflators. With respect to readymade garments, silk, carpets and coir textiles corresponding

price deflators were not available. These data have been deflated by using the deflator

of textiles. The analysis of export performance has been done with regard to the

change in the composition of exports and destination of exports. In order to understand

the change in the composition of exports during pre and post MFA period, annual

growth rate and Compound Annual Growth Rate has been calculated for the period from

1990 to 2012.

RESULT AND ANLAYSIS

This section describes the changes in Indian textile exports in terms of share of

textiles exports, composition and direction of textile exports.

Table 2: Growth rate and Descriptive statistics for Indian Textile Exports

|

Year

|

Phase

|

Value at Constant price (Rs in Millions)

|

Annual Growth Rate

|

Share to Total Exports (in %)

|

CAGR

|

|

PRE MFA PERIOD

|

|

|

1990-91

|

PHASE - I

|

131.01

|

-

|

17.65

|

16.49

|

|

1991-92

|

187.53

|

43.15

|

20.78

|

|

1992-93

|

234.38

|

24.98

|

23.63

|

|

1993-94

|

222.27

|

-5.16

|

18.59

|

|

1994-95

|

250.15

|

12.54

|

19.82

|

|

|

|

|

|

|

1995-96

|

271.77

|

8.64

|

18.17

|

|

1996-97

|

358.48

|

31.91

|

21.90

|

|

1997-98

|

429.55

|

19.82

|

24.66

|

|

|

|

|

1998-99

|

PHASE - II

|

422.25

|

-1.71

|

23.55

|

6.05

|

|

1999-00

|

479.28

|

13.51

|

24.04

|

|

2000-01

|

568.86

|

18.69

|

23.10

|

|

2001-02

|

534.10

|

-6.11

|

21.51

|

|

|

|

|

2002-03

|

PHASE - III

|

638.58

|

19.56

|

21.63

|

-3.09

|

|

2003-04

|

658.80

|

3.17

|

20.50

|

|

2004-05

|

581.23

|

-11.77

|

15.02

|

|

PRE MFA PERIOD

|

MEAN (Rs in Millions)

|

397.88

|

|

|

Standard Deviation (S.D) (Rs in Millions)

|

174.84

|

|

|

Coefficient of variation (C.V)

|

43.94

|

|

|

Compound Annual Growth Rate (CAGR) (in %)

|

10.44

|

|

|

POST MFA PERIOD

|

|

|

2005-06

|

PHASE – IV

|

726.18

|

24.93

|

15.91

|

5.72

|

|

2006-07

|

779.89

|

7.40

|

14.76

|

|

2007-08

|

770.23

|

-1.24

|

13.32

|

|

2008-09

|

892.16

|

15.83

|

12.77

|

|

2009-10

|

882.50

|

-1.08

|

12.84

|

|

2010-11

|

922.72

|

4.56

|

10.50

|

|

2011-12

|

1044.90

|

13.24

|

9.94

|

|

2012-13

|

1133.48

|

8.48

|

10.20

|

|

POST MFA PERIOD

|

MEAN (Rs in Millions)

|

894.01

|

|

|

Standard Deviation (S.D) (Rs in Millions)

|

140.20

|

|

|

Coefficient of variation (C.V)

|

15.68

|

|

|

Compound Annual Growth Rate (CAGR) (in %)

|

5.72

|

|

Source: Researcher’s calculation based on data from RBI

Table 2 depicts the CAGR and change in the share of textile exports to total exports

from 1990-91 to 2012-13. It is also evident from the table that the CAGR of textile

exports were higher during the pre MFA period (10.44) compared to post MFA (5.72).

Textile exports recorded a negative growth rate in the years of 1993-94, 1998-99,

2001-02 and 2004-05 in the pre MFA period. During 2001-02, the share of textile

exports to total exports recorded a negative growth rate compared to the previous

year. This could be attributed to the slowdown in the economies of some of the major

importing countries such as US, one of the largest trading partners for Indian textile

products and increasing competition from our neighboring countries like China and

Bangladesh. Apart from this India faced the problem of inadequate supply of domestic

cotton and high prices of imported cotton during this period. Along with this, the

unilateral changes introduced by certain trading partners in their rules of origin

also could have adversely affected textile exports during this period. High price

of raw material, high transaction cost and the unfavourable exchange rate also could

have been the factors, which have influenced India’s textile exports in that year

(Annual reports, Ministry of Textiles, 2003)

If we look into the annual growth rate it can be seen that the annual growth of

textile exports recorded a sharp increase from (-11.77) in 2004-05 to 24.93 during

2005-06, the period immediately after the quota removal. After that, India could

not maintain the same momentum in the growth rate. This can be partly attributed

to the effect of economic turbulence in the major exporting market of EU, US and

Canada (Ministry of Textiles, 2009). Apart from this, in the post MFA period, India

is facing stiff competition from Vietnam and Bangladesh in US Market and Turkey

and Bangladesh in the EU market. Bangladesh enjoys duty free access to European

markets, while Indian firms have to pay 9.6 per cent duty on their exports. Labour

cost in Bangladesh is 25 per cent cheaper than in India and products made in Bangladesh

is 15 per cent cheaper than Indian products. Earlier, Bangladesh was known for its

cheap labour, now it is competing in terms of quality, variety and design (Yunus

and Yamagata, 2012).

In 2007-08, the share of textiles exports to total exports recorded a negative growth

of -1.24. During this time textile exports suffered badly due to a perceptible slowdown

of the US economy and the sharp appreciation of rupee by 15per cent against the

dollar. Although the rupee has depreciated sharply vis-à-vis the US dollar since

April 2008, the export prospects of the Indian textiles sector continues to be adversely

affected. Some of the reasons attributed to this decline are the financial sector

melt down and economic slowdown in international markets, liquidity crunch, increased

cost of production because of increasing raw material costs, power and other input

costs which have affected the profitability of textiles and garments units in India

and their exports (Annual Report, Ministry of Textiles, 2009). USA, the single largest

importer of textiles and clothing items, observed a negative growth of 13.22 per

cent and 10.3 per cent in its imports of T&C from the world and India, respectively

in 2009 (Ministry of Textiles, 2010). This could have adversely affected Indian

textile exports in the US market.

It can also be seen from table 2 that the average export of textiles during the

post MFA period (Rs.894.01 million) is higher compared to the pre MFA period (Rs.397.88

million). If we compare the fluctuations in the level of textile exports, it can

be inferred that exports during the post-MFA period was more consistent as coefficient

of variation (CV) was less during then (15.68) compared to pre MFA period (43.94).

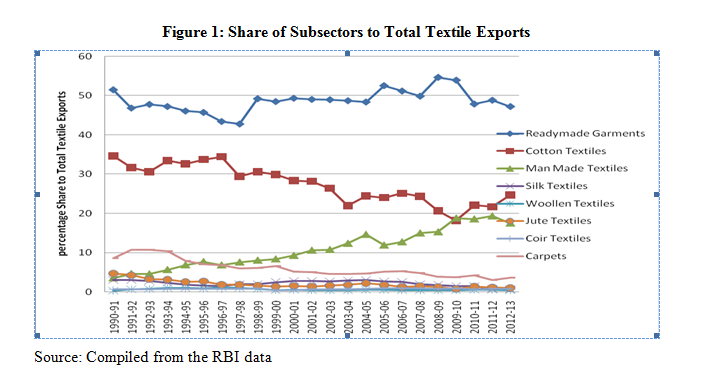

Figure 1: Share of Subsectors to Total Textile Exports

Source: Compiled from the RBI data

Figure 1 depicts the share of subsectors to total textile exports from 1990-91 to

2012-13. It can be seen that readymade garments constitute the largest share in

the overall textile exports accounting for more than 40 percent during the entire

analysis period. The share of cotton textile exports shows a slow declining trend

from 1997-98 to 2003-04. From 2005-06 onwards the share of this sector remains more

or less constant. The share of cotton textile exports to total exports was lowest

during 2009-10. This can be attributed to the decline in the production of cotton

fabrics, which constitute around 48 percent of the total fabric produced. Cotton

fabrics registered a yearly decline of over 17 percent during this time period (Ministry

of Textiles, 2009-10). The share of manmade textiles to total textile exports shows

an upward trend during the study period. This indicates the fact that there is a

marginal improvement in the share of manmade textiles to total textile exports during

the post MFA period. The above analysis points to the fact that readymade garments

still constitute the largest share of total textile exports from India. It is also

to be noted that the share of cotton textiles shows a marginal decline whereas the

share of manmade textiles shows a marginal increase during the post MFA period.

From this it can be concluded that the composition of textile exports have undergone

only a minor change in the post MFA period.

Table 3: Phase wise CAGR of subsectors of Indian Textile Exports under MFA

|

Year Sector

|

I Phase (1995-97)

|

II phase (1998-2001)

|

III Phase (2002-2004)

|

IV phase (2005-10)

|

|

Textiles (Excluding Readymade Garments)

|

16.49

|

6.05

|

-3.09

|

5.72

|

|

Readymade garments

|

13.94

|

5.96

|

-3.47

|

4.33

|

|

Cotton Textiles

|

11.27

|

3.88

|

-5.52

|

6.08

|

|

Manmade Textiles

|

15.8

|

13.54

|

7.32

|

10.94

|

|

Woollen Textiles

|

19.38

|

-7.03

|

6.67

|

3.6

|

|

Jute Textiles

|

2.46

|

2

|

7.76

|

-1.16

|

|

Silk Textiles

|

22.95

|

15.23

|

0.19

|

-11.95

|

|

Carpets

|

15.23

|

-2.55

|

3.93

|

4.1

|

|

Coir Textiles

|

10.75

|

0.78

|

-2.32

|

1.01

|

Source: Researcher’s calculation based on data from RBI

Table 3 shows the CAGR of subsectors of Indian textiles under different phases of

MFA. If we compare the CAGR of overall textile exports under different phases, it

can be seen that textiles as a whole recorded the highest CAGR in I phase (16.49

percent). If we compare this with the IVth phase (post MFA), the growth

has come down to 5.72 percent. A comparison of the CAGR of the different subsectors

in I phase shows that the highest CAGR was recorded in the silk textiles (22.95

percent) followed by woollen textiles (19.38 percent) and manmade textiles (15.8

percent). In the II phase, also silk textiles (15.23 percent) recorded the highest

CAGR followed by manmade textiles (13.54 percent) and readymade garments (5.96 cent).

In the III phase, most of the subsectors recorded a negative CAGR except manmade

textiles, woollen, jute, silk and carpets. This may due to the impact of recession

in US economy, which is one of the major export destinations for Indian textiles.

In the IV phase (post MFA), highest CAGR was recorded in manmade textiles (10.94

percent) followed by cotton textiles (6.08 percent) and readymade garments (4.3

percent). Likewise, if we compare the CAGR across the different phases it can be

seen that all the sectors recorded highest CAGR in the I phase compared to other

phases. This indicates the fact that in the liberalized trading regime India is

losing its position to its competitors. One of the areas where India could have

lost out to competitors is in terms of the integrated production facility. Countries

that have emerged globally competitive have a significantly consolidated supply

chain (Bharath textiles.com, 2013).

The elimination of quotas has opened new vistas for the international market for

textile and clothing export especially for the developing economies. Most of the

reviews cite US and EU as the two major trading partners for Indian textile products.

In the given background table 2 portrays the change in the destinations of Indian

textile exports during the pre and post MFA period.

Table 4: Destination for Indian Textile Exports- Pre and Post MFA Analysis

|

Sectors

|

Pre MFA (%)

|

Post MFA (%)

|

|

Textiles (Excluding Readymade Garments)

|

USA (21.4) UK (9.2) Germany (8.8)

|

USA (20.6) UAE (8) Bangladesh (6.82)

|

|

Readymade Garments

|

USA (33.94) Germany (9.99) UK (9.71)

|

USA (28.72) UK (12.35) UAE (9.23)

|

|

Cotton Textiles

|

USA (24.33) Bangladesh (11.9) UK (11.47)

|

UAE (14.3) Japan (10.17) Egypt (6.6)

|

|

Manmade Textiles

|

UAE (27.23) UK (10.09) Italy (6.48)

|

UAE (16.84) Turkey (8.64) Italy (3.3)

|

|

Woolen Textiles

|

UK (34.59) USA (18.22) Japan (16.28)

|

Italy (30.4) UK (27.09) USA (11.03)

|

|

Jute Texiles

|

Belgium (27.08) USA (24.3) UK (11.99)

|

USA (17.9) UK (10.61) Turkey (9.23)

|

|

Coir Textiles

|

USA (32.6) UK (10.91) Netherlands (10.1)

|

USA (32.2) China (10.3) Netherlands (8.2)

|

|

Carpets

|

USA (42.64) Germany (26.86) UK (4.89)

|

USA (42.41) Germany (16.81) UK (6.47)

|

Source: Compiled from Economic Outlook, CMIE.

Table 4 depicts the change in the destinations of Indian textile exports with respect

to different subsectors. India’s major textile destinations for textiles (excluding

readymade garments) during the pre MFA period were USA (21.4 per cent), UK (9.2

percent), Germany (8.8 percent), UAE (8 per cent) and Bangladesh (5.9 percent).

During the post MFA period, USA remained as the major textile exports destinations

with a share of 20.62 per cent. However, the share of USA has decreased from 21.4

per cent in the pre MFA period to 20.62 per cent in the post MFA period. A decrease

in the share of US can be attributed to lower domestic demand and increased imports

from preferential trading partners. An interesting trend in the post MFA period

is that UK which was holding the second position in terms of destination with a

share of 9.2 in the pre MFA period has come down to the 7th position

with a share of 4.7 per cent in the post MFA period. UAE that had a share of 8 per

cent in the Pre MFA period could improve its position as the second most important

destination with a share of 7.67 per cent followed by Bangladesh (6.82) and Germany

(5.73).

In the case of readymade garments, the major export destinations during the pre

MFA period were USA (33.94 per cent), Germany (9.99 per cent), UK (9.71 per cent)

followed by UAE (7.82 percent) and France (7.65 percent). Post MFA analysis shows

that the share of US in Indian garment imports has come down from 33.94 per cent

to 28.72 per cent. However, US still could maintain its rank as the largest importer

of Indian readymade garment products. In 2008-09, US, single largest importer of

Indian textile products observed a negative growth rate of 0.55 per cent in its

imports of textiles from India. This has reduced the Post MFA share of US in Indian

textile imports. One of the most remarkable shifts in the trend of Indian apparel

trade is that UK, which was in the third position with a share of 9.71 per cent

during Pre MFA period, has improved its position as the second largest importer

of Indian textiles in the Post MFA period with a share of 12.35 per cent. This shows

the compensatory gain of India in EU market at the expense of US during the post

MFA period. The share of UAE in the Indian garment imports has increased from 7.82

per cent during the pre MFA to 9.23 per cent. This is a clear indication that India

has taken the step to diversify its export market to other countries rather than

depending on US and EU alone.

India’s major trading destinations of cotton yarn, fabrics and made ups were USA

(24.33 per cent), Bangladesh (11.9 per cent), UK (11.47 per cent) followed by Germany

(8.13 per cent) and Hong Kong (7.82 per cent) during the pre MFA period. UAE, a

non quota country which had a share of 5.28 per cent in the pre MFA period became

the largest destination for cotton textiles in the post MFA period with a share

of 14.3per cent followed by Japan (10.17 per cent), Egypt (6.6 per cent), Turkey

(6.27 per cent) and Bangladesh (5.83 per cent). USA, which was the single largest

destination in the pre MFA period, has come down to ninth position in terms of import

destination with a share of 3.55per cent. This clearly shows that India has diversified

its export market in the post MFA period by exporting to different countries, including

the non-quota member countries.

Major destinations of manmade textiles during the pre MFA period were UAE (27.23per

cent), UK (10.09 per cent), Italy (6.48 per cent), Saudi (6.47 per cent) followed

by Turkey (5.95 percent) and USA. Share of UAE has decreased to 16.84 per cent in

the post MFA period. But it still remains as the largest destination for Indian

manmade imports. Turkey, which had a share of 5.95per cent during pre MFA period,

has increased its share to 8.64 percent to become the second largest destination

for manmade imports. UK, which was the second largest importer of manmade textiles

during the pre MFA period, has relegated to the 8th position in terms of its imports

from India. Likewise, Italy, which had a share of 6.48 per cent before 2005, has

experienced a decrease in its share to 3.3per cent during post MFA period.

India’s major woolen textiles export destinations were UK (34.59 per cent), USA

(18.22 per cent), Japan (16.28 per cent) followed by Italy (14.57 per cent) and

UAE (6.67per cent). An interesting observation during the post MFA period is that

Italy, which had a share of 14.57 per cent, has increased its share to 30.40 per

cent to become the single largest destination for Indian woolen exports. UK, which

was the largest destination for woolen exports with a share of 34.59 per cent during

pre MFA period, has moved to the second position with a share of 27.09 per cent

during the post MFA period.

In the case of jute textiles, during the pre MFA period, Belgium was the highest

destination for exports with a share of 27.08 per cent, followed by USA (24.3 per

cent), UK (11.99 per cent), Turkey (9.55 per cent) and Egypt (6.89 per cent). Belgium,

which was the largest single destination for Indian jute exports during the pre

MFA period, experienced a decline in their imports share after the removal of quota.

Share of Belgium imports has come down to 8.4 per cent thereby occupying the sixth

important position as the destination for Indian jute imports during the post MFA

period. Other major export destinations also experienced decline in their import

share. In the post MFA period, USA became the largest destination for jute exports

with a share of 24.3 per cent. Even though USA has become the largest importer of

jute products USA’s share has decreased to 17.9 per cent and UK experienced a marginal

decline in their import share 10.61 per cent. At the same time, India was able to

improve its market share in countries like Egypt and Saudi to the extent of 8.52

per cent and 9.23 per cent respectively. A decline in the share of major destinations

like Belgium, USA and UK may be due to the predominance of Bangladesh in these markets.

(Ministry of Textiles, 2010).

A comparison of the coir exports destinations during the pre and post MFA period

shows the USA has been remaining as the single largest destination for Indian coir

exports with a share of 32.6 per cent (Pre MFA) and 32.2 per cent (post MFA) respectively.

At the same time UK, which had a share of 10.9 per cent during the pre MFA period,

has experienced a decline in their share to the extent of 7.9 per cent in the post

MFA period. China, which had an import share of 0.03 per cent during the pre MFA

period, has experienced a huge increase in their share to the extent of 10.3 and

became the second largest destination for Indian coir exports during the post MFA

period. This may be due to the Export Market Development Assistance scheme initiated

by the government to improve the performance of coir textile exports in the international

markets China mainly uses this yarn to manufacture value added products and export

to other countries, including India. This has improved the Chinese demand for coir

textiles from India (Coir board, 2014).

With regard to the carpet export destinations, USA maintained as the largest trading

partner during the entire study period followed by Germany and UK. In the case of

Germany and UK, the share has come down in the post MFA period.

CONCLUSION

The above analysis throws light upon the fact that India could marginally improve

her performance in the post MFA period. A comparison of the CAGR during the study

period shows that textile exports as well as the sub sector exports showed a low

CAGR in the post MFA period compared to pre MFA. In terms of the CAGR, highest growth

was recorded in the manmade textiles followed by cotton textiles in the post MFA

period. Total textile exports also show a low CAGR in the post MFA period.

An important observation that emerges from the study is that USA could maintain

its position as the largest destination for Indian textile exports in the segment

of textiles, readymade garments, coir and carpets even during the post MFA period.

Even though USA remains as the largest export destination in the post MFA period,

the share of India exports to USA has come down in the post MFA period. This contradicts

the results of the previous studies which has projected India to increase its market

share in the US in the post MFA period (Exim Bank, 2005). Emergence of UAE as the

single largest destination for cotton textile exports is another important noteworthy

observation in the post MFA period.

Even though India could improve the performance after the quota removal, the present

analysis shows that the gain of Indian textiles and clothing exports in the post

MFA era have not been commensurate with its expectation. In the international markets

India is facing stiff competition from a host of countries especially Bangladesh,

Vietnam and China. Indian textile exports are suffering because raw materials are

phenomenally high priced. This makes the end product expensive by 15-30 per cent

than other competing markets. Also, the presence of more low end and low value added

items in India’s export basket also would have affected the competitiveness of Indian

textiles in the international market. The absence of contemporary designing facilities

and the failure to provide quality value added fabrics and garments act as a hindrance

for India to move up in the value chain. In order to improve the export performance,

India needs to continue pushing its exports to non-traditional emerging markets

of Africa, Asia CIS and Latin America. Indian textile industries inherent strength

such as availability of raw materials, especially cotton, integrated operations

and design skills would favour the shift of world export of textile industry to

India.

REFERENCES

Ananthakrishnan, P., & Jain-Chandra, S. (2005). The impact on India of trade

liberalization in the textiles and clothing sector. International monetary fund

(IMF).

Bharath Textiles. (2013). Indian Textile Exports: Post-MFA Scenario Opportunities

and Challenges. http://www.bharattextile.com/

Chadha, R., Pohit, S., Stern, R. M., & Deardorff, A. V. (1999). Phasing out

the Multi-Fibre Arrangement: Implications for India. Global Trade Analysis Project

(GTAP) at Purdue University.

Cline, W. R. (1990). Chapter 12: Textile and Apparel Negotiations in the Uruguay

Round: an Evaluation of the Proposals. Institute for International Economics.

Corporate Catalyst India Pvt Limited, (CCI) . (2015). A Brief Report on Textile

Industry in India. July 2015.

dhallenge

CMIE. Economic Outlook. Various issues. Center for Monitoring Indian Economy Pvt.

Ltd, Mumbai.

Coir Board. (2014). Evaluation Study of Domestic Market Development Assistance Scheme

implemented by Coir Board. Coir Board.

Exim Bank: Research Brief. (2005). Textile Exports: Post MFA Scenario Opportunities

and Challenges, No.11, Feb., online available at www. Eximbankindia.com. pp. 1-4.

Kathuria, S., Martin, W. and Bhardwaj, A. (2001). Implications for South Asian countries

of abolishing the multifibre arrangement, World Bank Working Paper 2721, Washington,

D.C. www.worldbank.org

Landes, Maurice ,Stephen Macdonald,Santosh K.Singh and Thomas Vollrath .(2005).

Growth Prospects for India’s Cotton and Textile Industry, CWS-05d-01, Economic Research

Service, US Dept. of Agriculture.

Martin, W. and Winters, L.A. (1996).The Uruguay Round and Developing Countries,

Cambridge University Press, Cambridge, pp.216-250.

Mehta, R. (1997). Trade Policy Reforms, 1991-92 to 1995-96: Their Impact on External

Trade. Economic and Political Weekly, 779-784.

Nanda, P., & Raikhy, P. S. (2001). WTO, Environmental and Labour Standards and

India's Textile Exports—Some Implications. WTO and the Indian economy, 298-311.

Ministry of Textiles Annual report. (2003-04). available at:

http://apparel.indiamart.com/annual-report/highlights.html.

Ministry of Textiles Annual report. (2008-09). available at: http://apparel.indiamart.com/annual-report/highlights.html.

Ministry of Textiles. (2009-10).Annual Report, Available at

http://texmin.nic.in/texpolicy

Ramachandran, V. (2001). Export Competitiveness and the Market for Textiles: A Summary

of Research. Harvard Studies – 7, Harvard University, January.

RBI .( Various Years). Data base on Indian Economy. Available at

http://dbie.rbi.org.in/

Singh, Narendra and Surinder S. Kundu. (2005). An analysis of the Competitive Dimensions

of Indian Cotton Textile Industry. Foreign Trade Review. Vol. XL No.1 (April-June)

pp 70-86.

Spinanger, D. (1999). Textiles Beyond the MFA Phase‐Out. The World Economy,

22(4), 455-476.

Verma, Samar. (2002). Export Competitiveness of Indian Textile and Garment Industry.

ICRIER, November. Working Paper No.94 pp 1-43.

World Trade Organization (WTO). International Trade Statistics, Various Issues.

Geneva.

Yunus, M., & Yamagata, T. (2012). The garment industry in Bangladesh, Chapter

6, Experience of Asia and Africa (Interim Report). Chousakenkyu Houkokusho, IDE-JETRO.

[1] Market disruption’’ was defined as instances of

sharp import increases associated with low import prices not attributable to dumping

or subsidies (Cline, 1990).