A Refereed Monthly International Journal of Management

Determining the Role of Employee’s Perception towards CRM Practices and Customer

Retention

|

Suhail Ahmad Bhat

Research Scholar

The Business School

University of Kashmir

Hazaratbal, Srinagar-190006

Contact No.- +91-9596498734

Email: ahmadsuhail@kashmiruniversity.ac.in

|

Dr. Mushtaq Ahmad Darzi

Professor

The Business School

University of Kashmir

Hazaratbal, Srinagar-190006

Contact No.- +91-9419089086

Email:mushtaqbs@gmail.com

|

Abstract

CRM and customer retention have increasingly being recognizedas important managerial

functions especially in saturated and increasingly competitive markets. Every business

firm knows that it costs far less to hold on the existing customer than to acquire

new ones. There is limited research available that investigates the effect of customer

knowledge and orientation on customer retention in banking sector. In this backdrop

the study tries to determine the impact of employee perception towards CRM practices

(customer knowledge and customer orientation) on customer retention. Structural

Equation Modelling (SEM) has been employed on a sample of 204 respondents who were

randomly selected from the population of employees of a particularbank in the Jammu

and Kashmir. Finding of the study revealsthat customer knowledge and customer orientationhas

significantly positive impact on the customer retention. This paper contributes

to the theory by evaluating the role of knowledge management and customer oriented

behaviour in developing long-term relationships with the customers. It also analyses

the importance of CRM practices for developing better customer retention strategies

in the banking sector where NPA rate is continuously increasing.

Keywords: Customer retention, customer knowledge, customer relationship

management, employee perception.

Introduction

After the economic recession of 2009-2011 resulting from global financial crisis,

businesses have slowly gaining the momentum. One of the prime causes of the recession

was unsecured loans provided by financial institutions which give rise to corrosion

of trust and commitment towards the customers (Vella and Caruana, 2012). This has

further resulted in a huge customer lossin the banking sector. Peppers and Rogers

(1996) have observed that most of the organizations might lose 25% of their existing

customers if proper customer retention strategies are not implemented. This was

further acknowledged by Pareto’s 80/20 Law that top 20 percent of customers

contribute 80 percent of profits to the businesses and are cash cows for the organizations.

Therefore, banks need to focus on their existing customers rather than achieving

cost leadership as competition isbeing observed a real threat to them (Biederman,

2010). Banks that want to achieve higher profitability need to retain the top 20

percent of customers by satisfying and preventing them from defecting. Happy cows

can give more milk but the irony is how to reveal if cows are happy. The answer

to this question lies in the fact that banks need to understand and analyse ‘cow

sociology’.This can be made possible by acquiring information and knowledge

about customers and their behaviour patterns, and customizing the bank offerings

according to customer needs (Lin et al., 2009). Consequently, Customer Relationship

Management (CRM) emerged as a strategic tool, which utilizes customer information

for maintaining and enhancing customer relationships. Understanding the customer’s

profitability and retaining profitable customers had been recognized as the core

value of customer relationship management (Hawkes, 2000).

Wang et al. (2010) argued that the fundamental aim of CRM is to improve the degree

of satisfaction and retention among customers through proper analysis of customer

knowledge thereby improving the overall corporate competitiveness of a firm. Drucker

(1954) opined that the main purpose of business is to acquire and retain customers.

This philosophy can be made operational by employing right CRM strategy, which synchronizes

people, process and technology components of a firm. Two main drives viz; customer

knowledge and customer orientation have been identified by most of the researchers,

which determine the effective implementation of CRM strategy(Yim et al., 2004; Raman

et al., 2006; Akroush et al., 2011; Wang and Feng , 2012; Elkordy, 2014). Reichheld

(1996) has argued that customer retention rates and customer share are important

metrics in CRM. An enhanced relationship with customers can help in accomplishing

greater retention and loyalty (Ngai, 2005). There is dearth of literature available

on the role of customer knowledge and orientation towards customer retention. No

empirical study has been conducted so for, which studies knowledge, orientation

and retention together in banking sector. One of the important contributions of

the study is that it can prove a remedy against the alarming NPA rate in India and

particularly in the state of Jammu and Kashmir.

Statement of Problem

The current market scenario of the banking sector is highly complex and competitive

with little stability due to the entry of national and international financial institution

in the emerging economies. The major aggravation in the industry is about obtaining

and retaining the customers. It has become a challenging task for a particular bank

to gain profits due to the fact that big fishes in the banking sector have dominated

the market. Market strategies in the nature of mergers, acquisitions, joint ventures

etc. have been adopted by the banks to reduced competition. But still the banks

are not able to achieve expected results. Reserve Bank of India has recently released

a report on banking sector profits which depicts that most of the private sector

banks have incurred loss in their previous fiscal years. One of the reason being

the increasing level of non-performing assets (NPA) and loan defaulters. As on March,

2015, the Gross NPA rate of public sector banks (PSBs) in India was 5.20 percent

which has gone up to 6.02 percent as of June, 2015. However, the Gross NPA rate

in the Jammu and Kashmir in 2014 was 4.73 percent and has gone up by more than one

percent to 5.81 which accounts for Rs. 2187 crores in 2014 to Rs. 2658 crores in

2015. The reason for such an NPA rate being that bank is not able to understand

its customer, which results in the breach of trust between the customer and bank.

This has brought in the issue of customer focus to the forefront. To understand

the credit worthiness of a customer bank has to develop an intimate relationship

with customers. It has to capture and assimilate all the information and knowledge

about the customer by employing right CRM strategy. The banks also need to redesign

their CRM strategy periodically to deliver quality services and maintain the existing

portfolio of customers in order to survive in the market. Therefore, an immediate

need is felt to study and evaluate the best CRM practices and their role in enhancing

customer retention in banking sector.

Objectives

The study has been carried out with the following objectives;

- To study the perception of employees towards CRM practices and customer retention

in banking sector.

- To determine the impact of customer knowledge and customer orientation on customer

retention.

Literature Review and Hypothesis Development

CRM has been conceptualized by different researchers in different way. Chan (2005)

has conceptualized CRM by integrating business processes, organizational structures,

analytical structures and technological representation to present a unified and

comprehensive view of a customer. Another study has put forward a conceptual model

of CRM effectiveness consisting of four customer-centric dimensions viz. customer

knowledge, interaction, value, and satisfaction (Kim et al., 2003). The researchers

further argued that CRM involves understanding and meeting customer’s unique

needs through business interactions. Thurau (2004) has argued that service personnel

customer-orientation has direct effect on the customer retention. The author has

put forth two reasons, firstly customer are willing to return again to companies,

whose service providers are customer-oriented because they like the staff that are

more customer-oriented. Secondly, customers are more influenced by the service staff

and reflect this trust to the whole company. Further, the author has linked service

personnel customer-orientation to the customer satisfaction, commitment and retention

(Thuran, 2004).

CRM has been viewed as a complex and holistic concept, which requires proper business

processes and integrated systems that enhances growth of a firm by developing strong

bonds of trust and commitment between customers and employees to enhance customer

satisfaction and retention (Xu et al., 2002).CRM practices can help the bank in

retention of existing customers in the competitive markets (Hugar and VazD'Costa,

2010). Proper CRM practices can potentially impact customer satisfaction rating

and can enhance customer retention. Benton and Maloni (2005) argued that CRM has

positively affected the productivity, profitability and efficiency of banks but

there is also a need to detect bank frauds. Al-Khouri (2012) has suggested some

common dimensions of CRM framework viz. key customer focus, knowledge management,

CRM organization and technology based CRM. These dimensions have a significant impact

on the customer retention and sales growth of a firm (Yim et al., 2004). It has

been concluded by some researchers that long-term relationship between customers

and banking organizations can be improved when service personnel’s have more

readiness towards customer orientation (Palmer and Bejou, 1994; Williams and Attaway,

1996; Beatty et al., 1996).Boveand Johnson (2000) opines that customer-oriented

service personnel, havinga high level of working knowledge, can efficiently recognize

customer’s needs and aspirations and can fulfil them in a desirable manner

(Thurau, 2004). Verhoef (2003) has found that both the customer’s desire to

extend his/her relationship with the institution and his reliance on the customer-loyalty

programs positively affect customer retention and the growth of customer’s

share.

Customer knowledge management is one of the important processeswhich utilize various

knowledge management concepts and technologies in capturing the customer knowledge

for developing better relationships (Gebert, 2002).Customer knowledge plays an important

role in responding to customer needs by acquiring customer information and knowledge

through technology based software (Wood, 2003). According to Kotler and Armstrong

(2008), the main aim of any organization should go beyond attracting new customers

and creating value for them but it should also include retaining existing customers.

Knowledge Management is one of the important dimensions of CRM that enables it to

move from mechanical, data-driven technology approach to a comprehensive and holistic

customer knowledge management system (Gebert, 2002). Customer retention has been

considered as one of the important outcomes of seller-buyer relationship (Crosby

et al., 1990). Retaining customers is important for long-term growth and sustainability

of the business. It is cheaper to keep current customers than to find new ones (Harley,

1984). The previous literature has theoretically and empirically linked customer

relationships to customer retention (e.g. Jackson, 1985; Kumar et al., 1995). A

variety of CRM activities can work together to enhance customer retention (Pfeifer

and Farris, 2004).

In the light of above discussion, there is very scarcity of literature both theoretical

and empirical, to study the variables viz. customer knowledge, orientation and retention

together in developing economies. Therefore, the study tried to determine the impact

of customer knowledge and orientation on customer retention in banking sector. On

the basis of above literature following hypothesis has been formulated;

H1: Customer knowledge has a significantly positive impact on customer

retention.

H2: Customer orientation has a significantly positive impact on

customer retention.

Methodology

Proposed Model

The proposed model for the study was developed based on the research problem and

the already available literature on CRM and associated concepts. As shown in Figure-1,

the model has two independent variables i.e. customer knowledge and customer orientation

which influence the customer retention that is presumed as independent variable.

The hypotheses are based on this model and in order to test these, a survey has

been conducted on the employees of a bank operating in the state of Jammu and Kashmir.

Figure 1: Conceptual Model

Sample and Data Collection

The data has been collected from the employees of a bank in Jammu and Kashmir. The

particular bank was chosen for the study as having taken a lead in the adoption

of CRM in the state of Jammu and Kashmir. Simple random sample technique was adopted

to collect the data from the total population of employees of the bank in the state.

Data was collected in the year 2014-15 from a sample of 204 employees. However,

a total of 225 questionnaires were distributed among the respondents consisting

of 12 items but only 204 were received back from them, thus the overall response

rate was 91 percent. Before the collection of final data, a pilot study was performed

on 25 bank employees to ensure face validity and content validity of the questionnaire.

Some items were droppedandmodified which the respondents were not able to understand

easily. The sample size was determined on the basis of following criteria;

- Most researchers consider a sample size of 200-500 respondents adequate for most

of management researches (Hill and Alexander, 2000; Tabachnick and Fidell, 2001).

- The sample size can be determined on the basis of number of items in questionnaire

for each item 5 to 10 respondents are adequate (Hair et al., 1998).

Sample Description

The sample characteristics are given in Table-1. The table reveals that the sample

has high percentage of Male respondents (53.5 percent) than female respondents (46.6

percent). Highest percentage of respondents was observed from Kashmir region (52.9

percent) than Jammu region (47.1 percent). Among various designations in the bank,‘Personal

Banker’ (23.5 percent) has highest percentage and ‘Back up Manager’

(12.7 percent) has lowest percentage. The other designations include ‘Assistant

Managers’ (18.6%), ‘Branch Sales Officers’ (17.7%), ‘Branch

Managers’ (14.3), and ‘Relationship Managers’ (13.2 percent).

The ‘Personal Banker’ is a key person in the bank as maximum responsibility

towards the banking functions are performed by him/her. Also highest percentage

of respondents was observed from the experience group of ‘3-5 years’

and lowest number was found in the ‘above 9 years’ group.

Table 1: Demographic Description of Sample

|

Demographic Variables

|

Category

|

Frequency

|

Percentage

|

|

Gender

|

Male

|

109

|

53.4

|

|

Female

|

95

|

46.6

|

|

Region

|

Kashmir

|

108

|

52.9

|

|

Jammu

|

96

|

47.1

|

|

Designation

|

Branch Manager

|

29

|

14.3

|

|

Back-up Manager

|

26

|

12.7

|

|

Personal Banker

|

48

|

23.5

|

|

Relationship Manager

|

27

|

13.2

|

|

Assistant Manager

|

38

|

18.6

|

|

Branch Sales Officer

|

36

|

17.7

|

|

Experience (yrs.)

|

Below 1yr

|

10

|

4.9

|

|

1-3 yrs.

|

58

|

28.4

|

|

3-5 yrs.

|

78

|

38.2

|

|

5-7 yrs.

|

35

|

17.2

|

|

7-9 yrs.

|

18

|

8.8

|

|

9 yrs. Above

|

5

|

2.5

|

Questionnaire Design and Development

The research instrument for the study has been divided into two sections. The first

section contains demographic description of the respondents like gender, region,

designation and experience. The respondents were supposed to write their personal

details at the appropriateplace provided for each question. Second section contains

items/statements related to the various variables identified in the study i.e. customer

knowledge, orientation, retention. The respondents were asked to give their response

on five-point Likert scale (1-5), ranging from 1 (strongly agree) to 5 (strongly

disagree). The items of the questionnaire were developed from the existing questionnaire

items developed by the researchers. Some modifications were made to suit the objectives

of the present study. The itemised scale is given in Annexure-I.

Reliability and Validity Analysis

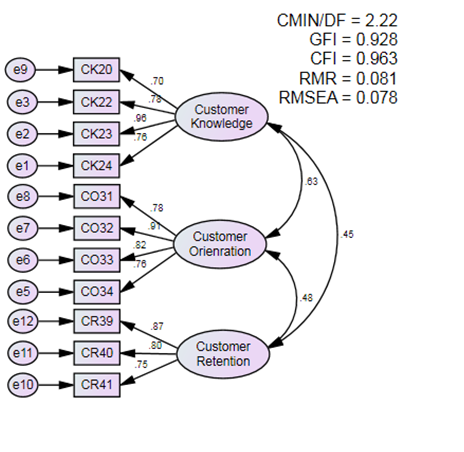

Confirmatory factor analysis (CFA) was adopted to examine the reliability and validity

of the measurements. A measurement model was developed for the constructs consisting

of variables as customer knowledge, orientation and retention as shown in Figure-2.

After examining the model summary of measurement it was observed that the fit indices

are in the acceptable range and it fits the data well (Figure-2). The threshold

for model fit includes, CMIN/DF (< 2 is good and 2 – 4 acceptable); Goodness-of-fit

Index (GFI> 0.90 is good and > 0.80 acceptable); Comparative Fit Index (CFI

> 0.90); Root Mean Residual (RMR < 0.10) and Root Mean Square Error of Approximation

(RMSEA < 0.10) (Chau, 1997). Furthermore, a factor loading of the constructs

with their items was determined from the measurement model and the items with loading

below 0.70 were droppedand a loading above 0.60 has also been acceptable by reserachers

(Hair et al., 1998).

Figure 2: Measurement Model

On the basis of item loadings, convergent validity of the research instrument was

determined that includes average variance extracted (AVE), construct reliability

(CR) and discriminant validity (DV) as shown in Tables-2. The threshold for AVE

should be 0.5 or above; CR should be 0.7 or above to indicate adequate convergence

or internal consistency.For DV, the square of the correlation between factors should

not exceed the variance extracted (Fornelland Larcker, 1981), which indicates the

degree to which measures of conceptually distinct construct differ.

Table 2: Factor Loadings of CFA

|

Latent Variables

|

Scale Items

|

Path Estimate*

|

Average Variance Extracted

|

Construct Reliability

|

|

Customer Knowledge

|

CK20

|

0.70

|

0.65

|

0.88

|

|

CK22

|

0.78

|

|

CK23

|

0.96

|

|

CK24

|

0.76

|

|

Customer Orientation

|

CO31

|

0.78

|

0.67

|

0.89

|

|

CO32

|

0.91

|

|

CO33

|

0.82

|

|

CO34

|

0.76

|

|

Customer Retention

|

CR39

|

0.87

|

0.65

|

0.85

|

|

CR40

|

0.80

|

|

CR41

|

0.75

|

*All the paths are significant at p < 0.05; Source: AMOS Output

Table-2 reveals that the loadings of all the items are above the threshold of 0.70

but item CK21 from customer knowledge construct was dropped because of loading below

0.70. The three constructs have AVE and CR above the acceptable limit suggested

by Nunnally and Bernstein (1994). The table-3 shows discriminant validity results,

diagonal variance of constructs are given and are above the square correlation between

the variables in the table.

Table 3: Discriminant Validity Results

|

|

CK

|

CO

|

CR

|

|

CK

|

0.65a

|

|

|

|

CO

|

0.40

|

0.67a

|

|

|

Paste Correlations Table into A1 and Standardized Regression Weights Table

into F1 , then click me.

|

CR

|

0.20

|

0.23

|

0.65a

|

Note: a Variance Extracted

Results and Discussions

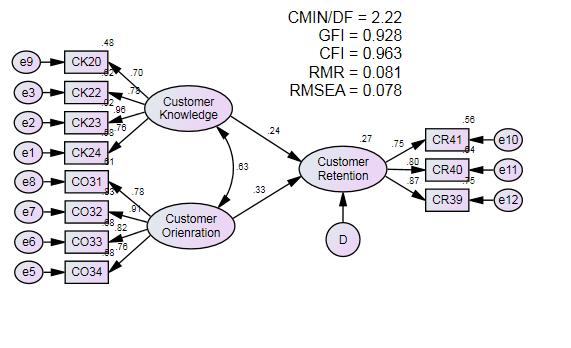

SEM has been employed to determine the model fit of structural model and to test

the various hypotheses formulated in the proposed model. Maximum Likelihood (ML)

estimation with 5000 sub-samples bootstrapping procedure using AMOS 20 has been

used for testing the proposed hypotheses. The various model fit indices were estimated

and it was observed that the model fits the data well. CMIN/DF of the model is 2.22;

GFI is 0.928; CFI = 0.963; RMR = 0.081 and RMSEA being 0.078 as shown in Figure

3. The model fit indices are above the acceptable range and reveal that the structural

model is in conformity to the proposed model.

Figure 3: Structural Model

The hypotheses were tested through evaluation of regression estimate, critical ratio

(CR), level of significance (p-value). For the current study 5 percent significance

level has been set. The results are shown in Table-4, which reveals that the path

from customer knowledge to customer retention has regression weight of 0.24; CR

of 2.48 and p-value of 0.013. These parameters are above the threshold and provide

support to the hypothesis H1 that customer knowledge has a significantly positive

impact on customer retention. Further, the path from customer orientationto customer

retention has regression weight of 0.33; CR of 3.33 and significant at 0.01, which

provide support to the second hypothesis H2 that customer orientation has a significantly

positive impact on customer retention. The coefficient of determination (R-square

is 0.27) in the model reveals that 27 percent of variance in customer retention

is explained by customer knowledge and customer orientation. However, there might

be some other variables that will explain rest of variance in the customer retention.

Table 4: Results of Structural Model

|

Paths

|

Std. Estimates

|

Critical Ratios (CR)

|

P-value

|

Decision

|

R2

|

|

CR

|

<---

|

CK

|

0.24

|

2.48

|

0.013

|

H1 Supported

|

0.27

|

|

CR

|

<---

|

CO

|

0.33

|

3.33

|

***

|

H2 Supported

|

|

Notes: *** p-value < 0.01

|

Source: AMOS Output

The study has empirically validated the two key dimensions of customer retention

i.e. customer knowledge and customer orientation. It has been found that customer

knowledge has a significant positive impact on the customer retention. Through customer

knowledge management the bank can keep its customers informed about the latest benefits

and offers regarding their products and services. The bank can be able to understand

the needs of customers by encouraging two-way communication between customers and

employees.Knowledge management when used in combination with information technology

can help in acquiring customer data that can become a source of competitive advantage

for the firm. Valuable information regarding the purchase behaviour of customer

can be retrieved from the data. This information can be used to customize the bank

offerings according to the customer needs and preferences resulting in better and

more profitable relationships. Thus customer knowledge management can aid in retention

of existing customer and acquiring new customers. These findings are in context

with the earlier findings which depicts that the customer knowledge has a significant

impact on the retention of customers (Wood, 2003; Pfeifer and Farris, 2004; Wang

et al., 2010).

The finding of the study also reveals that customer orientation has positive impact

on customer retention. Employees while adopting customer oriented approach in a

bank can track the customer complaints and can effectively address them. Customer

oriented personnel can provide information to customers regarding the new services

and developments in the existing services regularly. The service personnel can also

provide support to the customers while utilising services of the bank. Therefore,

it has reconfirmed the findings of earlier studies which have found that customer

focused service or customer oriented services play an important role in facilitating

mutual relationship between organizations and their customers (Varki and Colgate,

2005; Gan et al., 2006). The results, again, are in consistence with the earlier

findings which reveal that different CRM practices can work together to enhance

customer retention (Pfeifer and Farris, 2004). Thus the findings of the study indicate

that the banks that are able to understand their customers and manage customer information

properly are in a better position to prevent customer defection.

Conclusion

The study attempts to determine the perception of bank employees towards the CRM

practices and their subsequent impact on customer retention. It has empirically

proved the inter-relationship between CRM practices and customer retention. Two

prominent CRM practices highlighted by the study include customer knowledge and

customer orientation that have significantly positive impact on the customer retention.

In addition it has been discovered that CRM has a potential to create value for

the customer in long run.The customer knowledge captured through systematic gathering

of uncluttered feedback from customers on continual basis helps everyone in the

organization ranging from front-line employees to branch manager in understanding

the customer’s experience to the bank service. Organizations need not only

to take pulse of customer opinions but should strategize to correct weaknesses,

fine-tune their offerings and motivate employees towards relationship development

in both monetary and non-monetary terms. Customer orientation is more important

for developing and maintaining relationship with customer as the study has empirically

proved. So, banks need to adopt customer-centric approach and should prioritize

customer retention. While developing and implementing retention strategies, the

banks should consider the nature of product/service to be sold, type of customer

to be retained and objectives of the owners. By taking these conditions into consideration,

banks can have more individualistic and customized retention strategies.

Implications

The study has established a positive relationship between customer orientation,

knowledge and retention and provides some implication to managers. The Marketing

Personnel has a profound role in connecting bank to the customers as they are in

direct touch with the customers. Their attitude towards customer affects the perception

of customer towards the bank. Marketing staff with strong customer orientation are

more likely to create favourable perception of the bank in the mind of customers

thereby enhancing customer retention.

The managers should give more emphasis on promoting customer-oriented values and

behaviours among employees that will encourage in developing customer-oriented culture

in the bank. Managers need to periodically assess the level of customer-oriented

behaviour of its employees and should make efforts to maintain a friendly, supportive

working environment in the bank. Also training programs and reward systems should

be designed in such a way that promotes customer orientation among employees.

Limitations and Future Research

The findings of the study are applicable to one single bank only as the data has

been collected from one bank only. So the results of this study should be cautiously

generalised. This study can be extended to other banks or organizations as well.

The data has been collected from employees only, customers and other stakeholders

associated with CRM have not been taken. Future research should consider all the

stakeholders associated with CRM. The study uses a cross-sectional research design

however, for better understanding of customer behaviour longitudinal design should

be employed. As the finding of study reveal that only 27 percent of variance in

customer retention is explained by customer knowledge and customer orientation,there

might be some other variables which will explain more of variance in the dependent

variable.

References

Akroush, M.N., Dahiyat S.E., Gharaibeh H.S. and Abu-Lail, B.N. (2011). Customer

relationship management implementation: An investigation of a scale’s generalizability

and its relationship with business performance in a developing country context.

International Journal of Commerce and Management, 21(2), 158-191.

Al-Khouri, A.M. (2012). Customer relationship management: proposed framework from

a government perspective. Journal of Management and Strategy, 3, 34-54.

Beatty, S.E., Mayer, M., Coleman, J.E., Reynolds, K.E. and Lee, J. (1996). Customer-sales

associates retail relationships. Journal of Retailing, 73(3), 223-247.

Benton, W.C. and Maloni, M. (2005).The influence of power driven buyer/seller relationships

on supply chain satisfaction, Journal of Operations Management, 23, 1-22.

Biederman, D. (2010). The customer is king, again. The Journal of Commerce,

May, available at: www.nrsonline.com/pdfs/JOC.pdf.

Bove, L.L. and Johnson, L.W. (2000).A customer-service worker relationship model.International

Journal of Service Industries Management, 11(5), 491-511.

Chan, J.O. (2005). Toward a unified view of customer relationship management.Journal

of American Academy of Business, 6(1), 32-8.

Chau, P. (1997). Re-examining a model for evaluating information center success

using a structural equation modeling approach.Decision Sciences, 28(2),

309-333.

Crosby, L.A., Evans, K.R. and Cowles, D. (1990). Relationship quality in services

selling: an interpersonal influence approach. Journal of Marketing, 54(7),

68-81.

Drucker, P. (1954). The Practice of Management.Harper and Row, New York, NY.

Elkordy, M. (2014).The Impact of CRM Capability Dimensions on Organizational Performance.European

Journal of Business and Social Sciences, 2(10), 128-146.

Fornell, C. and Larcker, D.F. (1981).Evaluating structural equation models with

unobservable variables and measurement error.Journal of Marketing Research,

18, 39-50.

Gan, C., Cohen, D., Clemes, M. and Chong, E. (2006). A survey of customer retention

in the New Zealand banking industry: banks and bank systems. Journal of Business

Research, 1, 83-99.

Gebert, M., Probst, G., and Leibold, M. (2002).Five Style of Customer Knowledge

Management and How Smart Companies Use them to Create Value. European Management

Journal, 20(5), 459-469.

Hair, J., Anderson, R., Tatham, R. and Black, W. (1998).Multivariate Data Analysis,

5th ed., Prentice-Hall, Upper Saddle River, NJ.

Harley, D.R. (1984). Customer satisfaction tracking improves sales, productivity,

morale of retail chains. Marketing News, June, p. 15.

Hawkes, V.A. (2000). The heart of the matter: the challenge of customer lifetime

value. CRM Forum Resource.

Hill, N. and Alexander, J. (2002).Handbook of Customer Satisfaction and Loyalty

Measurement, Second Edition, Gower Publishing Company, Hampshire.

Hugar, S.S. and Vaz (D'Costa), N.H. (2010). A model for CRM implementation in Indian

public sector banks.International Journal of Business Innovation and Research,

4(1), 143-162.

Jackson, B.B. (1985). Winning and Keeping Industrial Customers: The Dynamics of

Customer Relationships, Lexington Books, Lexington, MA.

Kim, J., Suh, E. and Hwang, H. (2003).A model for evaluating the effectiveness of

CRM using the balanced scorecard.Journal of Interactive Marketing, 17(2),

5-19.

Kotler, P. and Armstrong, G. (2008).Principles of Marketing.(12th edn), McGraw-Hill,

New York.

Kumar, N., Scheer, L.K. and Steenkamp, J.E.M. (1995).The effects of perceived interdependence

on dealer attitudes.Journal of Marketing Research, 32(8), 348-356.

Lin, N-H., Tseng, W-C., Hung, Y-C.and Yen, D.C. (2009). Making customer relationship

management work: evidence from the banking industry in Taiwan. The Service Industries

Journal, 29(9), 1183-1197.

Ngai, E.W.T. (2005). Customer relationship management research (1992-2002): an academic

literature review and classification. Marketing Intelligence & Planning,

23(6), 582-605.

Nunnally, J.C. and Bernstein, I.H. (1994).Psychometric Theory, 3rd ed., McGraw-Hill,

New York, NY.

Palmer, A. and Bejou, D. (1994). Buyer-Seller Relationships: A Conceptual Model

and Empirical Investigation. Journal of Marketing Management, 10, 495-512.

Peppers, D. and Rogers, M. (1996). The one to one future: Building relationships

one customer at a time, 102–122.

Pfeifer, P.E. and Farris, P.W. (2004). The elasticity of customer value to retention:

the duration of a customer relationship. Journal of Interactive Marketing,

18, 20-31.

Raman, P., Wittmann, C.M. and Rauseo, N.A. (2006).Leveraging CRM for Sales: The

Role of Organizational Capabilities in Successful CRM Implementation.The Journal

of Personal Selling and Sales Management, 26(1), 39-53.

Reichheld, F.F. (1996). The Loyalty Effect, Harvard Business School Press, Boston,

MA.

Tabachnick, B.G. and Fidell, L.S. (2007). Using Multivariate Statistics, (5th ed.)

Pearson: Boston.

Thurau, T. (2004). Customer Orientation of Service Employee… International

Journal of Service Industry Management, 15(5), 460-478.

Varki, S. and Colgate, M. (2005).The role of price perceptions in an integrated

model of behaviour intentions.Journal of Service Research, 3, 232-240.

Vella, J. and Caruana, A. (2012). Encouraging CRM systems usage: a study among bank

managers. Management Research Review, 35(2), 121-133.

Verhoef, P.C. (2003). Understanding the Effect of Customer Relationship Management

Efforts on Customer Retention and Customer Share Development.Journal of Marketing,

67(4), 30-45.

Wang, F., Hu, F. and Yu, L. (2010).The application of customer relationship management

in investment banks.Asian Social Science, 6(10), 178-183.

Wang, Y. and Feng, H. (2012). Customer relationship management capabilities: Measurement,

antecedents and consequences. Management Decision, 50(1), 115 – 129.

Williams, M.R. and Jill S.A. (1996).Exploring Salesperson’s Customer Orientation

as a Mediator of Organizational Culture’s Influence on Buyer-Seller Relationships.Journal

of Personal Selling & Sales Management, 16(4), 33-52.

Wood, R.A. (2003). Customer Knowledge Management.Knowledge Roundtable.

Xu, Y., Yen, D.C., Lin, B. and Chou, D.C. (2002), Adopting customer relationship

management technology, Industrial Management and Data Systems, 102(8), 442-452.

Yim, F. Hong-Kit, Anderson, R.E. and Swaminathan, S. (2004). Customer relationship

management: Its dimensions and Effect on Customer Outcomes. Journal of Personal

Selling and Sales Management, 24(4), 263-278.

Annexure I

Customer Knowledge (Yim et al., 2004; Arnett and Badrinarayanan,

2005; Sin et al., 2005; Khodakarami and Chan, 2014)

CK20. The bank provides channels to enable on-going two-way communication

between customers and employees.

CK21. The customers are kept informed about the latest benefits

and offers regarding various products and services.

CK22. The bank fully understands the needs of customers.

CK23. Bank always provides statements with accurate data.

CK24. Our bank offers overdraft facility to the high net-worth.

Customer Orientation (Bowen et al., 1989; Jayachandran et al.,

2005; Evans et al., 2007; Donnelly, 2009; Elkordy, 2014)

CO31. Our bank has access to 24*7 helpline for receiving complaints

from the customers.

CO32. The bank provides access to information regarding banking

services via internet and mobile.

CO33. The bank has the mechanism to evaluate the customer-centric

performance standards at all customer touch points.

CO34. The bank has not enough resources and expertise for the successful

relationship development.

Customer Retention (Yim et al., 2004; Schweidel et al., 2008; Chinje,

2013)

CR39. The feedback is taken from customers on regular (weekly)

basis.

CR40. The customer is empowered through personalized messages which

encourage healthy relations.

CR41. Bank has a culture where customer is given first preference.