Sustainability Reporting- A Recent

Trend and Future Prospects in India

|

Anand Rai

Associate Professor

Finance, School of Management

JRE Group of Institutions

Greater Noida (U.P.)

|

Abstract

Climate change, social degradation, economic crisis and complexities

in business have raised serious concern over organisations' sustainability. Sustainability

reporting is a broad term considered synonymous with others used to describe

reporting on economic, environmental, and social impacts (e.g., triple bottom

line, corporate responsibility reporting, etc.). The purpose of a sustainability

reporting is the practice of measuring, disclosing, and being accountable to

internal and external stakeholders for organizational performance towards the

goal of sustainable development.

Currently in India, only few

companies have adopted such reporting practices as compared to other developed

countries like Japan, USA etc. With the growing concern on social and

environmental issues worldwide, this decade is going to see paradigm shift in

reporting standards on sustainability.

Global Reporting Initiative is a

non-profit organization that works towards a sustainable global economy by providing

sustainability reporting guidance. GRI pioneered and developed a comprehensive

sustainability reporting framework that is widely used around the world.

This article explores the guidelines of GRI’s

sustainability reporting standards. It also unveils recent reporting trends of

the Indian organisations on sustainability performances and future prospects.

Keywords:

Sustainability, Triple Bottom Line, GRI, Disclosure Frameworks, Corporate Social

Responsibility

Introduction

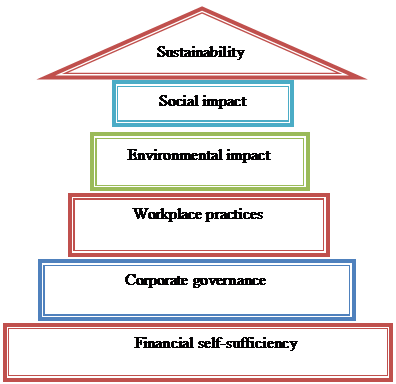

An organisation needs to

be financially self sufficient to be able to become sustainable in the long

term. Once this primary need for financial capital has been met, the

organisation then needs to be socially responsible. This is achieved by

ensuring that its governance and workplace practices and its environmental and

social impact are self monitoring and conform to society’s expectations and

ethical values. Only then a company can achieve sustainability in the long

term.

Figure 1:

Relationship between sustainability and financial self-sufficiency

Evolution of the concept of

Sustainability

In

1919, a landmark judgment was given by the Supreme Court of the State of

Michigan, USA in the case of Dodge v. Ford Motor Company. The court said that

the primary objective of a business is to make profits and that any business is

responsible to its shareholders and not to the community as a whole or to its

employees. To date this judgment is treated as a fundamental reference point in

relation to the responsibilities of a business and the inherent principle in it has not been overruled by

courts.

Nobel

Laureate Milton Friedman (1970) wrote that the responsibility of a business is

to

increase profits and that engaging in activities which discharge the corporate

social responsibilities (CSRs)

of a business is an instance of 'agency

conflict' or a conflict between managers and shareholders. Friedman explains

further that CSR activities are undertaken by

managers to their personal needs and at the expense

of the shareholders. Also, he even went on to say that in a free enterprise

society, CSR reflects an inappropriate use of corporate funds.

Since

the early 1980s, social scientists have moved away from the theory of agency as

propagated by Friedman and gravitated towards a new model developed by Peston

and Caroll, which was embodied in a structure they called the “corporate social

performance” (CSP) framework, which combines the principles and philosophy of

societal needs with the economic responsibilities of a business.

Freeman

(1984) defined stakeholders as “any group or individual who can affect or is affected

by the achievements of an organisation's objectives”. The stakeholder’s theory

asserts that firms have relationships with many constituent groups and that

these stakeholders both affect and are affected by the actions of the firm. In

1984, Freeman argued that the systematic attention of the stakeholders interest

is critical to the success of a firm and that management must pursue action that

are optimal for a broad class of stakeholders rather than those that serve only

to maximise shareholder interests.

These

principles set the path for more research and understanding of these theories and

led to the integration of the environmental, social and governance

responsibilities of a business with the otherwise predominant economic aspects.

The stakeholder concept has facilitated the inclusion of the sustainability

concept in the core business practices of a company.

Sustainability

Reporting

The

changing global environment is challenging companies to look beyond financial

performance to drive business. Business leaders are increasingly realizing the

need to integrate environmental and social issues within the business strategy.

In a world of changing expectations, companies must account for the way they

impact the communities and environments where they operate. Climate change, community

health, education and development, and business sustainability are some of the

most important issues of this decade. Businesses are increasingly involved in

these areas as are their clients and their people. This raises the importance

of accurately and transparently accounting for and reporting these activities.

Sustainability

means different things

to different people. The most often quoted definition is from the Brundtland Commission

(1987) which states that sustainable development is "Development that

meets the needs of the present without compromising the ability of future generation

to meet their own needs." Sustainability is, therefore, more of a journey

that a destination wherein ideals, values and measurement metrics are in a

constant state of evolution.

The Triple Bottom Line (TBL), a term coined by Elkington (l997) implies that corporation should

focus “not just on the economic value they add but also on the environmental and social value

they add – and destroy".

As Deegan (1999) indicated, “for an organisation or community to be

sustainable, it must be financially secured (as evidenced through such measures

as profitability), it must minimise (or ideally eliminate) its negative

environment impact, and it must act in conformity with society’s expectation”.

While Sustainability Reporting is a decade old idea, it is

relatively in its early years with the methodology evolving constantly. Still,

many nations and organizations have started to understand the concept and

incorporate it in their business functions. Sustainability Reporting is a

process for publicly disclosing an organizations economic, social and

environmental performance. As with any disclosure, the Sustainability Report

lays bare the organizations performance to public scrutiny. What distinguishes the

Sustainability Report from other reports is the fact that it makes an

organization look at its business from every possible quarter in a single

document. In an ideal world, the organization’s stakeholders would analyze the

report and give constructive feedback to the organization to improve its

performance.

But Sustainability Reports need to serve a purpose. It should be

possible to derive information and knowledge out of them so that they can be

compared across organizations. For this purpose, common standards need to be

developed. It was in this context that the Global Reporting Initiative (GRI) was

founded in 1997 as a project under Ceres, a Boston (US) based national network

of investors, environmental organizations and other public interest groups working

with companies and investors to address sustainability challenges such as

global climate change. In 2002, GRI became an independent international NGO and

its secretariat has since been located in Amsterdam, The Netherlands. Its main

role was to set up a multi-stakeholder process to define guidance to

organizations on what issues they should measure and report on. GRI pioneered and developed a comprehensive sustainability

reporting framework that is widely used around the world.

GRI reporting framework

Sustainability reports based on the GRI

Reporting framework disclose outcomes and results that occurred within the

reporting period in the context of the organization’s commitments, strategy,

and management approach. Reports can be used for the following purposes, among

others:

i)

Benchmarking and

assessing sustainability performance with respect to laws, norms, codes, performance

standards, and voluntary initiatives;

ii)

Demonstrating how

the organization influences and is influenced by expectations about sustainable

development; and

iii)

Comparing performance

within an organization and between different organizations over time.

The GRI Reporting Framework is intended to serve as a generally accepted framework for

reporting on an organization’s economic, environmental, and social performance.

It is designed for use by organizations of any size, sector, or location. It

takes into account the practical considerations faced by a diverse range of organizations

– from small enterprises to those with extensive and geographically dispersed

operations.

The GRI Reporting Framework contains

general and sector-specific content that has been agreed by a wide range of

stakeholders around the world to be generally applicable for reporting an

organization’s sustainability performance.

1. Standard Disclosures: The

Guidelines identify information that is relevant and material to most organizations

and of interest to most stakeholders. There are three different types of

disclosures suggested by GRI.

i)

Strategy and Profile: Disclosures

that set the overall context for understanding organizational performance such

as its strategy, profile, and governance.

ii)

Management Approach: Disclosures

that cover how an organization addresses a given set of topics in order to

provide context for understanding performance in a specific area.

iii)

Performance Indicators: Indicators

that elicit comparable information on the economic, environmental, and social

performance of the organization.

2.

Performance Indicators: The

Sustainability Performance Indicators is

organized by economic, environmental, and social categories. Social Indicators

are further categorized by Labour, Human Rights, Society, and Product

Responsibility. Each category includes a Disclosure on Management Approach and

a corresponding set of Core and Additional Performance Indicators. Core

Indicators have been developed through GRI’s multi-stakeholder processes, which

are intended to identify generally applicable indicators and are assumed to be

material for most organizations. An organization should report on Core

Indicators unless they are deemed not material on the basis of the GRI

Reporting Principles. Additional Indicators represent emerging practice or

address topics that may be material for some organizations, but are not material

for others. The Disclosure(s) on Management Approach should provide a brief

overview of the organization’s management approach to the Aspects defined under

each Indicator Category in order to set the context for performance

information. The organization can structure its Disclosure(s) on Management

Approach to cover the full range of Aspects under a given category or group its

responses on the Aspects differently.

2.1 Economic Performance Indicators:

The economic dimension of sustainability concerns

the organization’s impacts on the economic conditions of its stakeholders and

on economic systems at local, national, and global levels. The Economic

Indicators illustrate:

i) Flow of capital among different stakeholders; and

ii) Main economic impacts of the organization throughout

society.

Financial performance is fundamental to

understanding an organization and its own sustainability. However, this

information is normally already reported in financial accounts. What is often

reported less, and is frequently desired by users of sustainability reports, is

the organization’s contribution to the sustainability of a larger economic

system. Following are the economic performance indicators.

Aspect:

Economic Performance

EC1 (Core) :

Direct economic value generated and distributed, including revenues, operating

costs, employee compensation, donations and other community investments,

retained earnings, and payments to capital providers and governments.

EC2

(Core): Financial implications and other risks and opportunities for the

organization’s activities due to climate change.

EC3 (Core):

Coverage of the organization’s defined benefit plan obligations.

EC4

(Core): Significant financial assistance received from government.

Aspect:

Market Presence

EC5

(Add): Range of ratios of standard entry level wage by gender compared to

local minimum wage at significant locations of operation.

EC6

(Core): Policy, practices, and proportion of spending on locally-based

suppliers at significant locations of operation.

EC7

(Core): Procedures for local hiring and proportion of senior management

hired from the local community at locations of significant operation.

Aspect:

Indirect Economic Impacts

EC8

(Core): Development and impact of infrastructure investments and

services provided primarily for public benefit through commercial, in kind, or pro bono engagement.

EC9 (Add): Understanding

and describing significant indirect economic impacts, including the extent of

impacts.

2.2 Environmental Performance Indicators: The

environmental dimension of sustainability concerns an organization’s impacts on

living and non-living natural systems, including ecosystems, land, air, and water.

Environmental Indicators cover performance related to inputs (e.g., material,

energy, water) and outputs (e.g., emissions, effluents, waste). In addition, they

cover performance related to biodiversity, environmental compliance, and other

relevant information such as environmental expenditure and the impacts of

products and services.

Aspect: Materials

CoreEN1

(Core): Materials used by weight or volume.

EN2 (Core): Percentage

of materials used that are recycled input materials.

Aspect: Energy

EN3 (Core): Direct

energy consumption by primary energy source.

EN4 (Core): Indirect

energy consumption by primary source.

EN5 (Add): Energy

saved due to conservation and efficiency improvements.

EN6 (Add): Initiatives

to provide energy-efficient or renewable energy based products and services,

and reductions in energy requirements as a result of these initiatives.

EN7 (Add): Initiatives

to reduce indirect energy consumption and reductions achieved.

Aspect: Water

EN8 (Core): Total

water withdrawal by source.

EN9 (Add): Water

sources significantly affected by withdrawal of water.

EN10 (Add): Percentage

and total volume of water recycled and reused.

Aspect: Biodiversity

EN11 (Core): Location

and size of land owned, leased, managed in, or adjacent to, protected areas and

areas of high biodiversity value outside protected areas.

EN12 (Core): Description

of significant impacts of activities, products, and services on biodiversity in

protected areas and areas of high biodiversity value outside protected areas.

EN13

(Add): Habitats protected or restored.

EN14 (Add): Strategies,

current actions, and future plans for managing impacts on biodiversity.

EN15 (Add): Number

of IUCN Red List species and national conservation list species with habitats

in areas affected by operations, by level of extinction risk.

Aspect: Emissions, Effluents, and Waste

EN16 (Core): Total

direct and indirect greenhouse gas emissions by weight.

EN17 (Core): Other

relevant indirect greenhouse gas emissions by weight.

EN18 (Add): Initiatives

to reduce greenhouse gas emissions and reductions achieved.

EN19 (Core): Emissions

of ozone-depleting substances by weight.

EN20 (Core): NO,

SO, and other significant air emissions by type and weight.

EN21 (Core): Total

water discharge by quality and destination.

EN22 (Core): Total

weight of waste by type and disposal method.

EN23 (Core): Total

number and volume of significant spills.

EN24 (Add): Weight

of transported, imported, exported, or treated waste deemed hazardous under the

terms of the Basel Convention Annex I, II, III, and VIII, and percentage of

transported waste shipped internationally.

EN25 (Add): Identity,

size, protected status, and biodiversity value of water bodies and related habitats

significantly affected by the reporting organization’s discharges of water and

runoff.

Aspect: Products and Services

EN26 (Core): Initiatives

to mitigate environmental impacts of products and services, and extent of

impact mitigation.

EN27 (Core): Percentage

of products sold and their packaging materials that are reclaimed by category.

Aspect: Compliance

EN28 (Core): Monetary

value of significant fines and total number of non-monetary sanctions for

noncompliance with environmental laws and regulations.

Aspect: Transport

EN29 (Add): Significant

environmental impacts of transporting products and other goods and materials

used for the organization’s operations, and transporting members of the workforce.

Aspect: Overall

EN30 (Add): Total

environmental protection expenditures and investments by type.

2.3 Social

Performance Indicators: The social dimension of

sustainability concerns the impacts an organization has on the social systems

within which it operates. The GRI Social Performance Indicators identify key Performance

Aspects surrounding labour practices, human rights, society, and product responsibility.

2.3.1 Labour Practices and Decent Work Performance

Indicators

Aspect: Employment

LA1 (Core): Total

workforce by employment type, employment contract, and region, broken down by

gender.

LA2 (Core): Total

number and rate of new employee hires and employee turnover by age group, gender,

and region.

LA3 (Add): Benefits

provided to full-time employees that are not provided to temporary or part time

employees, by significant locations of operation.

Aspect: Labor/Management Relations

LA4 (Core): Percentage

of employees covered by collective bargaining agreements.

LA5 (Core): Minimum

notice period(s) regarding operational changes, including whether it is specified

in collective agreements.

Aspect: Occupational Health and Safety

LA6 (Add): Percentage

of total workforce represented in formal joint management–worker health and safety

committees that help monitor and advise on occupational health and safety programs.

LA7 (Core): Rates

of injury, occupational diseases, lost days, and absenteeism, and total number of

work-related fatalities, by region and by gender.

LA8 (Core): Education,

training, counselling, prevention, and risk-control programs in place to assist

workforce members, their families, or community members regarding serious

diseases.

LA9 (Add): Health

and safety topics covered in formal agreements with trade unions.

Aspect: Training and Education

LA10 (Core): Average

hours of training per year per employee by gender, and by employee category.

LA11 (Add): Programs

for skills management and lifelong learning that support the continued employability

of employees and assist them in managing career endings.

LA12 (Add): Percentage

of employees receiving regular performance and career development reviews, by

gender.

Aspect: Diversity and Equal Opportunity

LA13 (Core): Composition

of governance bodies and breakdown of employees per employee category according

to gender, age group, minority group membership, and other indicators of

diversity.

Aspect: Equal Remuneration for Women and Men

LA14 (Core): Ratio

of basic salary and remuneration of women to men by employee category, by significant

locations of operation.

LA15

(Core): Return to work and retention rates after parental leave, by

gender.

2.3.2 Human Rights: There

is growing global consensus that organizations have the responsibility to

respect human rights. Human rights Performance Indicators require organizations

to report on the extent to which processes have been implemented, on incidents

of human rights violations and on changes in the stakeholders’ ability to enjoy

and exercise their human rights, occurring during the reporting period. Among

the human rights issues included are non discrimination, gender equality,

freedom of association, collective bargaining, child labor, forced and

compulsory labor, and indigenous rights.

Human Rights Performance Indicators

Aspect: Investment and Procurement Practices

HR1 (Core): Percentage

and total number of significant investment agreements and contracts that include

clauses incorporating human rights concerns, or that have undergone human rights

screening.

HR2 (Core): Percentage

of significant suppliers, contractors, and other business partners that have

undergone human rights screening, and actions taken.

HR3 (Core): Total

hours of employee training on policies and procedures concerning aspects of

human rights that are relevant to operations, including the percentage of

employees trained.

Aspect: Non-discrimination

Core

HR4 (Core): Total

number of incidents of discrimination and corrective actions taken.

Aspect: Freedom of Association and Collective Bargaining

HR5 (Core): Operations

and significant suppliers identified in which the right to exercise freedom of association

and collective bargaining may be violated or at significant risk, and actions taken

to support these rights.

Aspect: Child Labor

HR6 (Core): Operations

and significant suppliers identified as having significant risk for incidents

of child labor, and measures taken to contribute to the effective abolition of

child labor.

Aspect: Forced and Compulsory Labor

HR7 (Core): Operations

and significant suppliers identified as having significant risk for incidents

of forced or compulsory labor, and measures to contribute to the elimination of

all forms of forced or compulsory labor.

Aspect: Security Practices

HR8 (Add): Percentage

of security personnel trained in the organization’s policies or procedures concerning

aspects of human rights that are relevant to operations.

Aspect: Indigenous Rights

HR9 (Add): Total

number of incidents of violations involving rights of indigenous people and

actions taken.

Aspect: Assessment

HR10 (Core): Percentage

and total number of operations that have been subject to human rights reviews

and/or impact assessments.

Aspect: Remediation

HR11 (Core): Number

of grievances related to human rights filed, addressed and resolved through

formal grievance mechanisms.

2.3.3 Society: Society

Performance Indicators focus attention on the impacts organizations have on the

local communities in which they operate, and disclosing how the risks that may

arise from interactions with other social institutions are managed and

mediated. In particular, information is sought on the risks associated with

bribery and corruption, undue influence in public policy-making, and monopoly

practices.

Society Performance Indicators

Aspect: Local Communities

SO1 (Core): Percentage

of operations with implemented local community engagement, impact assessments,

and development programs.

SO2 (Core): Operations

with significant potential or actual negative impacts on local communities.

SO3 (Core): Prevention

and mitigation measures implemented in operations with significant potential

or actual negative impacts on local communities.

Aspect: Corruption

SO4 (Core): Percentage

and total number of business units analyzed for risks related to corruption.

SO5 (Core): Percentage

of employees trained in organization’s anti-corruption policies and procedures.

SO6 (Core): Actions

taken in response to incidents of corruption.

Aspect: Public Policy

SO7 (Core): Public

policy positions and participation in public policy development and lobbying.

SO8 (Add): Total

value of financial and in-kind contributions to political parties, politicians,

and related institutions by country.

Aspect: Anti-Competitive Behavior

SO9 (Add): Total

number of legal actions for anticompetitive behavior, anti-trust, and monopoly

practices and their outcomes.

Aspect: Compliance

SO10 (Core): Monetary

value of significant fines and total number of non-monetary sanctions for

noncompliance with laws and regulations.

2.3.4 Product Responsibility: Product

Responsibility Performance Indicators address the aspects of a reporting

organization’s products and services that directly affect customers, namely,

health and safety, information and labelling, marketing, and privacy. These

aspects are chiefly covered through disclosure on internal procedures and the

extent to which these procedures are not complied with.

Product Responsibility Performance Indicators

Aspect: Customer Health and Safety

PR1 (Core): Life

cycle stages in which health and safety impacts of products and services are assessed

for improvement, and percentage of significant products and services categories

subject to such procedures.

PR2 (Add): Total

number of incidents of non-compliance with regulations and voluntary codes

concerning health and safety impacts of products and services during their life

cycle, by type of outcomes.

Aspect: Product and Service Labelling

PR3 (Core): Type

of product and service information required by procedures, and percentage of significant

products and services subject to such information requirements.

PR4 (Add): Total

number of incidents of non-compliance with regulations and voluntary codes concerning

product and service information and labelling, by type of outcomes.

PR5 (Add): Practices

related to customer satisfaction, including results of surveys measuring customer

satisfaction.

Aspect: Marketing Communications

PR6 (Core): Programs

for adherence to laws, standards, and voluntary codes related to marketing communications,

including advertising, promotion, and sponsorship.

PR7 (Add): Total

number of incidents of non-compliance with regulations and voluntary codes concerning

marketing communications, including advertising, promotion, and sponsorship by

type of outcomes.

Aspect: Customer Privacy

PR8 (Add): Total

number of substantiated complaints regarding breaches of customer privacy and losses

of customer data.

Aspect: Compliance

PR9 (Core): Monetary

value of significant fines for noncompliance with laws and regulations

concerning the provision and use of products and services.

Policy initiatives by Indian Government

on corporate social responsibility and sustainable development

With increasing importance of India as a global economy and its role

at crucial international forums dealing with economic and climate change

issues, the Finance Ministry decided in 2011 to expand the scope of the annual

Economic Survey to include a chapter on the topic of financing of climate

change. The survey discusses the effect of climate change in India, the government

initiatives, financing and overall strategy.

India has many

publicly-funded programs for the

prevention and control of climate risks and issues

relating to sustainable development. One of

the major objectives of many rural development and

poverty upliftment programmes is the reduction of vulnerability to risks

arising out of climate change.

Banks have been assigned a special role in the economic development

of the country, and the Reserve Bank of India, the banking regulator, has prescribed that certain percentage

of bank lending should be allocated to developmental sector called the “Priority

Sector”. In addition, banks have begun to realise their role as multipliers for

responsible and sustainable business as they increasingly integrate evaluation

on sustainability as one of the key inputs to their decision on financing and

valuation of projects. Similarly, the Charter on "Corporate Responsibility

for Environmental Protection (CREP)" from Ministry of Environment & Forest

(MoEF) looks beyond the compliance of regulatory norms for prevention & control

of pollution through various measures including waste minimisation, in-plant

process control & adoption of clean technologies. The Charter set targets

concerning conservation of water, energy, recovery of chemicals, reduction in pollution,

elimination of toxic pollutants, process & management of residues that are

required to be disposed of in an environmentally sound manner, listing action

points for pollution control for various categories of highly polluting industries.

Financial reporting in India includes mandatory reporting on environment and social

matters such as on consumption of energy, use of raw materials and intermediaries,

conservation efforts, accounting for environment cost, and disclosures on liability

for environment issues. Labour and industrial laws are also well established and

companies are required to report on matters such as salaries, wages and benefits

paid to employees and the status of payment towards retirement and social benefits.

The Ministry of Corporate Affairs released Voluntary Guidelines on Social, Environmental

and Economic Responsibilities of Business (NVGs) in July 2011 after considerable

stakeholder consultations. They are compatible with globally acceptable guidelines

on sustainability reporting. The GRI focal point India and the GIZ India have supported

and promoted the creation of the NVG through the IICA-GIZ CSR Initiative.

Recently, the department of public enterprises has issued guidelines on Sustainable

Development and CSR for Central Public Sector Undertakings (CPSEs). These guidelines

stipulate how much and how CPSEs should invest and report on Corporate Social Responsibility

(CSR). The CSR budget mandated range from 0.5 percent to 5 percent of the profit

depending on the net profit of the CPSE.

A recent decision taken by the Securities and Exchange Board of India (SEBI) mandates

that listed entities should submit Business Responsibility report as a part of their

annual reports, which would describe measures taken by them along the key principles

enunciated in the 'National Voluntary Guidelines on Social, Environmental and Economic

Responsibility of Business' (NVGs) framed by the Ministry-of Corporate Affairs (MCA).

To start with, this requirement would be applicable to the top 100 companies in

terms of market capitalisation and would be extended to other companies in a phased

manner. This decision indicates the importance that the Government of India places

on the fulfilment of environmental, social and governance responsibilities of businesses.

The new Company's Bill tabled in the Parliament in December 2011 is a key steps

towards strengthening corporate governance and business sustainability measures.

The new Bill suggest that Every company with a net worth exceeding Rs. 5 billion

or a turnover exceeding Rs. 10 billion or profit

exceeding Rs. 50 million should form a committee of three or more directors, including

at least one independent director, to recommend activities for discharging corporate

social responsibilities in such a manner that the company would spend at least 2

percent of its average profits of the previous three years on CSR. The company is

also required to disclose its activities in its report or on its website, and to

institute a formal policy on CSR.

Sustainability reporting trends in India and around the world

Indian companies have been reporting on sustainability since 2001 by using the

GRI Framework, following the Carbon Disclosure Project (CDP) or completing the UN

Global Compact's Communication of Progress (CoP). The process of evolution for most

companies has been to initiate the reporting process under the CDP or the UNGC CoP,

and later progress into reporting under the GRI Framework, which is based on both

principles and standard disclosures, including performance indicators. However,

a small number of companies report under all the three reporting norms. The number

of companies reporting on sustainability has been increasing but is still relatively

small as compared to the total number of companies that are publicly traded in India.

The first version of the GRI Guidelines was issued in 2000. A second generation

of the guideline known as G2 was unveiled in 2002 at the World Summit on Sustainable

Development in Johannesburg. Some Indian companies started reporting on the G2 framework

from the year it was launched in 2002. Since then, the number of reporting companies

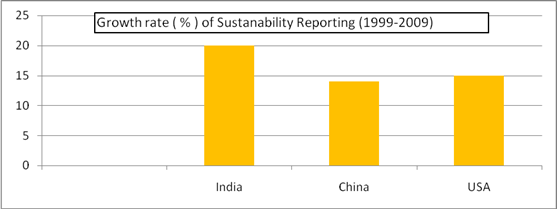

has increased steadily over the years. It can also be observed that the growth rate

of sustainability reporting is higher in India as compared to China and USA in the

period from 1999 to 2009.

Figure-2: Growth rate in Sustainability Reporting

Source: GRI Sustainability Report

GRI launched the third generation of its Guidelines, G3, in 2006 and Indian companies

transitioned to the G3 Guidelines in 2007; all reports since 2009 are based on the

G3 guidelines. In a recent analysis by GRI, it has been observed

that Indian companies are producing the highest proportion of complete report globally,

implying the disclosure of a complete set of information that is relevant to the

reporting organisation and external assurance. In March 2011, GRI published the

G3.1 guidelines - an update and completion of G3, with expanded guidance on reporting

gender, community and human rights- related performance - and Indian companies are

adapting to these new changes in the reporting framework. There are around 80 Indian

companies from various sectors that have been reporting and there

are about 60 companies that publicly declare that they

use the GRI guidelines, although only 74 sustainability reports are registered on

the GRI database. Most of these reports disclose information on almost all aspects

of performance indicators ranging from environment,

social and governance, although the rigour and details vary.

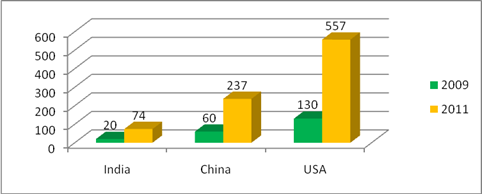

Figure-3: Number of Companies Reporting Sustainability

Source: GRI Sustainability Report

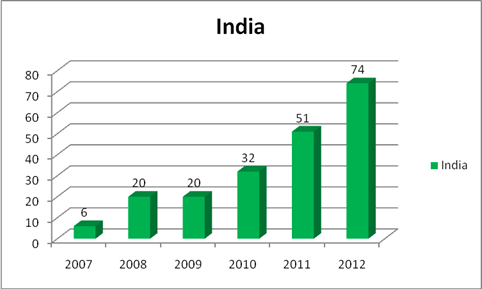

Figure-4: Number of Companies Reporting Sustainability in India

Source: GRI Sustainability Report

Issues with sustainability reporting

A recent study by University of Leeds and Euromed Management

School, France based on an analysis of over 4000 CSR reports

concluded that the reports have been fraught with irrelevant data, unsubstantiated

claims, and gaps in data and inaccurate data and suggest that missing rigour and

voluntary action results in lower public trust in such reports.

Unlike financial reporting, the disclosure of sustainability metrics to the market

is largely unregulated and predominantly voluntary. However, as sustainability becomes

a critical factor in the business environment it would become important for companies

to build a framework for these processes, information systems and controls that

match the quality and focus observed in financial reporting. A third party assurance,

in this direction, may ensure quality and consistency of disclosures. It involves

verification, which is an independent, documented and systematic process of scrutinizing

data, its associated processes and methods for collection and its management, which

leads to an assurance statement. This indicates the reliability of disclosures and

demonstrates credibility of the organization to its stakeholders.

Trends in external assurance of sustainability reports based on the GRI framework

from India reveals a rise in external assurance from 10% in 2006 to more than 70%

in 2010. This rise in percentage is significant more so when coupled with the rise

in number of GRI reports from Indian industry. It is worthwhile to note that GRI

recommends the use of external assurance

Conclusion

India is acknowledged as one of the fastest growing economies in the world; as

a result, it faces the challenge of balancing fuel consumption, and its rapid growth

with the equitable conservation of its key resources, and managing the impact on

society. Although corporate responsibility seems to be in the experimental

phase in India as of now, significant progress in both the number of reports and

quality of information reported is expected in the coming years. The expectations

form Indian reporters going forward is to focus on presenting information related

to:

i) Sustainability issues, challenges, dilemmas and opportunities.

ii) Regulatory environment and fact-based information.

iii) Information of interest to investors such as materiality

of issues in financial terms, vision and strategy statements, goals and targets,

etc.

iv) Explanation on identification and prioritization

of material issues.

v) Reader friendly report design.

At the regulatory level, various directives have been issued and with some still

in pilot stage. The Institute of Chartered Accountants of India (ICAI) has set up

the ICAI – Accounting Research Foundation (ICAI-ARF), which has undertaken a special

project to suggest a suitable framework for sustainability reporting for Indian

companies. Further, the Ministry of Corporate Affairs, Government of India in association

with the Indian Institute of Corporate Affairs has released the voluntary guidelines

on social, environmental and economic responsibilities of business. In the financial

sector, there is a visible trend to promote environmentally and socially responsible

lending and investment, with the Reserve Bank of India recently issuing a circular

for highlighting role of banks in promoting sustainable development.

There is no doubt that corporate responsibility is here to stay and businesses

have realized the value of embracing sustainability and more so making it a part

of their overall business strategy.

REFERENCES

Carroll, A., (1979), A three dimensional model of corporate performance, Academy

of Management Review, no. 4, pp. 99-120.

Deegan, C. (1997), “A Triple Bottom Line Reporting: A new approach for sustainable

Organisation” Charter, April, Vol.70, pp. 38-40.

Elington, J. (1997), “Cannibals with Forks: The Triple Bottom Line of 21st

Century Business”, Oxford Capstone Publishing.

Finch, Nigel (2005), “The Motivation for Adopting Sustainability Disclosure”,

MGSM Working Paper no. 2005-17, Available SSRN: http://ssrn.com/abstract=798724

Friedman, M., (1962), Capitalism and Freedom, University of Chicago Press,

Chicago.

Freidman, M., (1970), The social responsibility of business is to increase its

profits, New York Times, September 13, pp. 122-126.

Freeman, R. Edward (1984), Strategic Management: A Stakeholder Approach, Boston

Pitman, USBN 0273019139.

Gelb, D. and Strawser, J. (2001), "Corporate Social Responsibility and Financial

disclosure: An alternative explanation for Increased Disclosure”, Journal of Business

Ethics, Vol.33, No.1, pp. 1-13.

https://www.globalreporting.org/resourcelibrary/G3.1-Guidelines-Incl-Technical-Protocol.pdf

http://www.earthsummit2012.org/historical-documents/the-brundtland-report-our-common-future.

Mc William, A. and Siegel, D. (2001), “Corporate Social Responsibility: A Theory

of the Firm Perspective”, Academy of Management Review, Vol.1, No.26, pp.

117-27.