A Refereed Monthly International Journal of Management

Benefits and Challenges of Carbon Credit Trading practices in Organizations- A Case Study

Author

|

Ajay K. Garg

University Faculty (Tenure-Track),

Fairleigh Dickinson University,

842, Cambie Street, Vancouver, BC V6B 2P6 Canada

Email: ajaykgarg7@gmail.com

Cell: +1 604-362-2095

|

Satyendra Arya

Research Scholar,

Department of Management Studies,

TMIMT, Teerthanker Mahaveer University,

Moradabad-244001, Uttar Pradesh, India

Email: satyendra_arya17@rediffmail.com, satyendra.arya@gmail.com

Cell: +91- 9720169175 |

Rakesh K. Mudgal

Vice Chancellor,

Teerthanker Mahaveer University,

Moradabad-244001, Uttar Pradesh, India

Email: vicechancellor@tmu.ac.in

Cell: +91 9639644555 |

Abstract

Carbon Credit Trading is generated from the Kyoto Protocol. The main aim of this concept is basically to trade the carbon credit in the market. This type of trading is now the one of the fastest trading market in India. The companies that are not already carbon constrained will need to prepare themselves for carbon legislation as a low carbon economy in the long run. This research is used for the several benefits and challenges which are directly or indirectly associated with carbon credit trading. Some organizations are already taken lots of monetary and non-monetary benefits but nowadays several organizations are directly interested to involve in this trading. Carbon credits create a market for reducing greenhouse emissions by giving a monetary value to the cost of polluting the air. This means that carbon becomes a cost of business and is seen like other inputs such as raw materials or labor. The possibilities are endless; hence making it an open market. Operators that have not used up their quotas can sell their unused allowances as carbon credits, while businesses that are about to exceed their quotas can buy the extra allowances as credits, privately or on the open market. This research paper intends to explore the benefits and challenges about carbon credits amongst Indian Industry.

Keyword: Carbon Credit Trading, Kyoto Protocol, Clean Development Mechanism (CDM), Emerging Market.

Introduction

Emerging Concept: Carbon Credit

Carbon credits are basically an element which is used to aid in regulation of the amount of gases that are being released into the air. This isbasically a larger international plan which has been created in an effort to reduce global warming and its effects. This plan basically works by cappingthe amount of total emissions that can be released by one company or business. If there is a shortfall in the amount of gases that are used, there is a monetary value assigned to this shortfall and it may be traded. These credits are often traded between organizations or businesses. However, they also are bought and sold in international markets at whatever the determined market valuefor them is. There are also times when these credits are used to fund carbon reduction plans between trading partners.

Procedure of Carbon Credits Trading

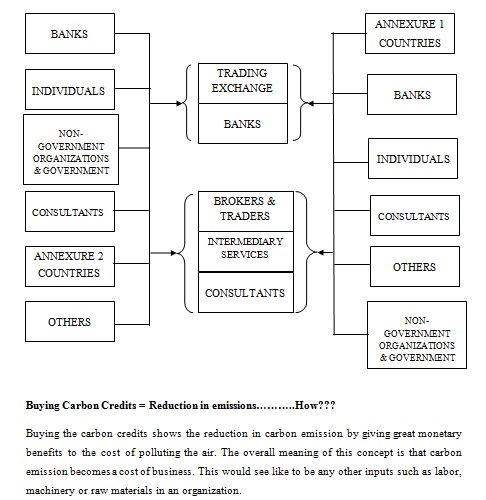

The procedure of carbon credits trading starts when a developed country is having comparatively high costs of domestic greenhouse gas reduction; to make a plan to set up a clean technology project in another developed or developing nation having a low cost of domestic greenhouse gas reduction. After the first stage, a developed country sets up a project in another developed or developing countries where the cost of carbon or greenhouse gas emission reduction project is comparatively low under the clean development mechanism. After setting up the project the developed country would receive carbon credits and another country would receive clean technology and some monetary benefits. At the end of this process, the country having carbon credits is allowed to sell their carbon credits in the global market under the international emission trading norms with the aim to quantify the emission reduction and limitation commitments under Kyoto Protocol. The basic procedure of carbon credit trading is shown in figure 1:

Sectors in which Carbon Credits can work

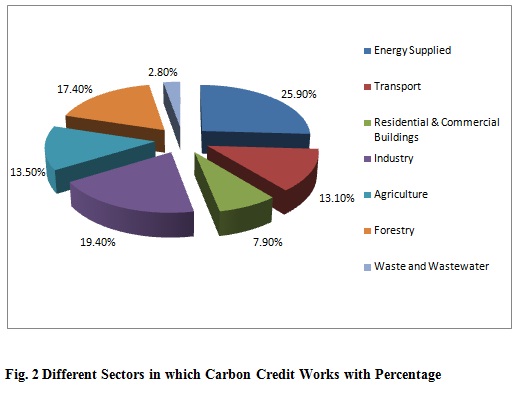

There are several sectors in which carbon credits work as shown in figure 2 and these are explained in the following paragraphs:

The energy is the most sensitive sector which is benefited by the carbon credits. The energy being major source of greenhouse gases and this can be benefited through carbon credits by providing alternate clean technology for energy production & supply. According to the data, the share is 25.90% of the total sectors involved.

Transportation sector is another sector which can be benefited by carbon credits. According to the above report, the share of transportation is 13.10%.

- Residential and Commercial Buildings

In these types of buildings, there are several sources of carbon generation such as consumption of electricity, use of various household products, etc. So, there are ample chances to involve the carbon credit. According to the assessment report, the weightage given to this category is 7.90%.

According to the data, industries have got the second position in the report. Now-a-days, there are several projects initiated by the industries for carbon credit trading. The share of this sector is 19.4%.

Governments of various countries are directly involved in this sector i.e. Agriculture. In India, lots of benefits are given to this sector by Government of India. According to the assessment report, the weightage goes to this sector is 13.50%.

Forests are the major source of greenery at our planet. So reforestation is the major thing on which the government must think over it. Another way to generate carbon credit is plantation of eco-friendly plants. According to the assessment report, the share of forestry is 17.40%.

Globally, now-a-days waste management is important sector to reduce carbon emission. So, there are lots of opportunities to earn carbon credits in this sector. With utilization of waste and wastewater emissions can also earn carbon credits. According to the data, the share is 2.8%.

Emerging Players avail benefits from Carbon Market:

There are several emerging players in India which are taking several benefits from carbon credit trading. Some of them are as follows:

- Gujarat Fluoro-chemicals Limited (GFL)

Gujarat Fluoro-chemicals Limited (GFL) is basically a part of the $2 billion INOX Group of Companies. INOX Group is managed business in diverse businesses including Industrial Gases, Refrigerants, Chemicals, Cryogenic Engineering, Renewable Energy and Entertainment. GFL had been at the forefront in bringing the concept of carbon credits to India. Its CDM project was the first project in the world to seek registration by the CDM Executive Board, a body of the United Nations Framework for Climate Change. GFL was the largest CDM player in India, and amongst the top 5 globally. In India, Gujarat Fluorochemicals Limited (GFL) has, over the years, earned a significant amount of revenue through sale of carbon credits in the global market. During financial year 2012-13, GFL posted revenues of around Rs 2,830 crore, of which carbon credit revenue was around Rs 876 crore (31 per cent). The company has witnessed a fall in its carbon credit revenue, over the years.

SRF with a turnover of $675 million (Rs. 4000 crore) is a multi-business entity engaged in the manufacture of chemical based industrial intermediates. Its business portfolio covers Technical Textiles, Fluorochemicals, Specialty Chemicals, Packaging Films and Engineering Plastics.

SRF gets carbon credits: A huge inventory now

SRF has been issued approx. 7.72 lakh carbon credit units by the issuing agency i.e. UNFCC. It has been issued approx 86.5 CERs. The price at which SRF sold the CERs is 22 Euro per CER.

The company's FY11 annual report mentioned Rs 64.17 crore received on account of carbon credits.

- Delhi Metro Rail Corporation (DMRC)

UN Body Credits Delhi Metro- 6.3 Lakh Carbon Credits for Modal Shift Project

The Delhi Metro Rail Corporation has been certified by the United Nations(UN) as the First Metro Rail and Rail based system in the world which will get carbon Credits for reducing Green House Gas Emissions as it has helped to reduce pollution levels in the city by 6.3 lakh tons every year thus helping in reducing global warming.

This organization will be ready to sell approx. $ 225 million worth of saved carbon. This is only possible with the help of blast furnace as well as corex furnace technology which is used in this plant. This technology prevents 15 million tons of carbon from being discharged into the atmosphere.

- Kalpatru Power Transmission Ltd.

Kalpatru Power Transmission Ltd's (KPTL) generates electricity from the mustard crop residues at its Rajasthan project. This is the first Indian project and the third project worldwide to which the UN panel issued carbon credits under the Kyoto Protocol. The Executive Board of the Clean Development Mechanism (CDM) had issued the first ever carbon credits or certified emission reductions (CERs) under the Kyoto Protocol in this category. These credits were issued for two hydroelectric projects in Honduras. CERs are generated by climate-friendly, sustainable development projects in developing countries. They can be used by developed country Governments and companies to meet their reduction commitments under the Kyoto Protocol. They can be traded and amount to one tonne of carbon dioxide equivalent. KPTL's Rajasthan project was the one of the top few Indian projects that were registered by the CDM panel at the United Nations Framework Convention for Climate Change.

Review of Literature

Trivedi S. (2016) explained about greenhouse gas or carbon market. This greenhouse gas market is increasing day-by-day. The researcher also told that this market is emerging several countries, different regions and corporate alliances around the globe. This new and emerging market offers effective risk management strategies for various organizations with emission constraints and substantial opportunities to organizations and their sponsors with emission reduction or clean development mechanism projects. His research also provide the brief overview regarding Kyoto Protocol, carbon credit trading, greenhouse effect and emerging greenhouse market and finally he also describe that how developing countries manage their energy resources or maximize their opportunities.

Kumar K.S.K. (2016) describe in his article about carbon taxes and carbon trading. He explains that both carbon taxes and carbon trading are market based instruments but they can be distinguished several criteria such as environmental effectiveness, simplicity, political acceptability, fiscal revenue and volatility. He also describe the defined procedure for the carbon trading which includes several steps such as Setting a Clear Goal – Capping Emissions, Assigning Responsibility – Allocating Allowances, Facilitating Cost-Effective Emission Reductions – Trading, Ensuring Accountability – Monitoring and Reporting and Ensuring Compliance – Reconciliation. Finally, the main focus of his research is cost effectiveness of carbon trading.

Fowler R. (2016) explains in his article about the several challenges and opportunities of carbon credits trading in agriculture industry. His main emphasis of his research on the farmers who are associated to the agriculture industry and directly or indirectly involve in carbon credits trading. He told that the Clean Development Mechanism (CDM) projects are best suited for controlling the carbon emission. The main challenge, which is faced by a crop producer, is the cost of measurement and verification of the change in carbon emissions. This concept is suited for the larger scale commercial farmers, especially when a group of neighboring farms is involved, can be reasonably and cost-effective, but for the small scale farmers, it is very difficult. Finally, he wanted to say that there are lots of opportunities exist even for small scale farmers in carbon credits trading and if they have a will then they grasp these opportunities.

Malav M. K., Kumar S., Malav L.C. and Kharia S. (2015) describe in their article about some monetary benefits of carbon credits trading. Their focus in article about the India’s role of carbon credits trading in the world’s carbon credits trading. Now, India qualifies to be a host country for the Clean Development Mechanism (CDM) projects and India is also considered as one of the most potential countries in the world for carbon credits trading through CDM projects. This can be possible only due to because in India, there are lots of opportunities in power sector and several proactive policies of the Indian government towards CDM. In this article, they also focus on the mechanism of carbon credit trading. Though Carbon Credit is definitely a very lucrative proposition for both the buying and selling countries, it is the environment which pays the heaviest price, as the GHG emitting countries cause environmental degradation by polluting it. So in that we have to be maintained a balance. This can only be done through sustainable development programs via renewable or zero carbon emission fuel.

Moukwa M. (2015) explains in his article about the enlisting market forces to the combat climate change in Carbon Credits Trading. His opinion that the approximately eighty two percent of the total world’s energy is still producing by the fossil fuels. So, there is still a long way to wean humanity off carbon, but carbon trading is a step forward. He believes that the greatest environmental threats that our planet faces today is the Earth’s climate and temperature patterns which is known as global climate change. Although fossil-fuel combustion has generated most of the buildup of climate-altering carbon dioxide (CO2) in the atmosphere, effective solutions require more than just designing cleaner energy sources. Equally important is the establishment of institutions and strategies, particularly markets, business regulations and government policies, which provide economies with incentives to apply innovative technologies and practices that reduce emissions of CO2 and other greenhouse gases.

Sethuraman N. R. (2014) explained about the carbon credit trading market and he also talked about the role of various solution providers. The finding of his research shows that the overall expenditure spent is approximately $300 to $ 500 by the developed countries for every ton reduction in carbon dioxide in comparison to $10 to $25 by the developing countries. Now-a-days the overall estimation of India’s greenhouse gas emission is below the target and this can be entitled to sell its surplus credits to the developed countries. In year 2010, India claimed about 31% of the total world carbon trade. This is the main reason that carbon credit trading is a hot trading market in India.

Singh N. (2014) describe in her article about Indian companies which are holding carbon credits stare at 'real loss'. She also explain about Indian companies, which had invested in clean development mechanism (CDM) projects under the Kyoto Protocol to claim certified emission reduction units (CER) or carbon credits, now stand to face a "real loss" on unsold credits, as opposed to a notional loss which was earlier being talked about, with prices falling below one euro. Industry estimates peg the notional loss at Rs 10,500 crore. So, this is a big challenge which are facing by Indian companies. The setting up of CDM projects served the purpose of controlling the rise in global temperature resulting in global warming. However, following the economic downturn, CER prices fell unexpectedly and there are still several companies which have failed to monetize on these credits even when prices were ruling around euro 10 in 2011. Indian CER holders are now looking forward to sell their CERs through validation and subsequent verification in certain other voluntary schemes. Anyone still holding CERs is at considerable loss, both notional and real. Most banks, trading companies and funds have closed their carbon desks, especially related to CER origination. There are limited options available to Indian CDM project developers but to sell at prevailing prices.

Patnaik N. (2012) describes that National Aluminium Company Limited (NALCO) is the first Public Sector Unit (PSU) in India that is dealing in carbon credits trading. This organization has established a project related to Carbon Sequestration. In its captive power plant at the place named Angul. The expectation from this project is basically to bring down the Green House Gases (GHG). After successfully implementing this project, NALCO will be getting all the benefits related to carbon credits trading. This can be done in the procedure of Carbon capturing from flue gas. These benefits may be availed through bio product and bio-energy generation.

Menon S. (2011) describes that there are several private investors who are ready to invest in clean development mechanism projects. They have made a strategy for earning profits from the CDM projects or by selling certified emission receipts or carbon credits. In this case, analysts expect that the CER prices should be same as in the European Union and in countries which further can encourage voluntary reduction in emission. So, it is the two way revenue stream that should be a help to private equity investors for participating in CDM projects as well as selling carbon credits.

Bhardwaj M. and Wadadekar A. (2010) explain in their article about Environmental Management. This is not simply managing the environment but it is the management of human interaction and an impact upon the environment in order to conserve for mankind’s sake. So, the biggest challenge in front of us is to manage the environment. To protect our environment, various governments create some law but these are not enough. In regarding this, one concept i.e. carbon credit trading, provides some ways to protect our environment and also provide some monetary benefits. According to industry estimation, Indian organizations are expected to generate approximately $ 8.5 billion at the going rate of $ 10 per tonne of Carbon emission Rating (CER). Reliance Energy is a company which already has energy efficiency and Clean Development Mechanism (CDM) projects and now Tata Sponge Iron Ltd. also got a CDM certificate from the United Nations (UN) for its waste heat recovery project in Orissa. So finally, various companies are taking some steps for creating our environment safe.

Research Objectives

- To know the basic concept of carbon credit trading.

- To analyze the basic procedure of carbon credit trading in India.

- To study the various benefits and challenges associated with carbon credit trading practices in organizations.

Research Methodology

A research methodology is the way of defining the activity of research, the procedure of research, determining the elements of such research in terms of scientifically adopted models or approaches, designs and tools. The Present study has made an attempt to fulfill the rational requirements of a scientifically conducted research to the maximum possible extent.

In this research, the researcher takes the analytical and descriptive research approach. The main population of this research is entire part of India and took 80 samples from a 400 to 500 organizations. The basic research tool in this research is questionnaire and the researcher took convenient and random sampling. The data in respect of research methodology of this research is as follows in table 1:

Table 1 Research Methodology

|

S. No.

|

Particulars

|

Data

|

|

1

|

Survey Area

|

India

|

|

2

|

Sample Size

|

87

|

|

3

|

Sample Unit

|

Organizations

|

|

4

|

Type of Research

|

Analytical & Descriptive Research

|

|

5

|

Sampling Type

|

Convenient and Random Sampling

|

|

6

|

Research Tool

|

Questionnaire

|

|

7

|

Data Type

|

Primary & Secondary Data

|

Data Analysis

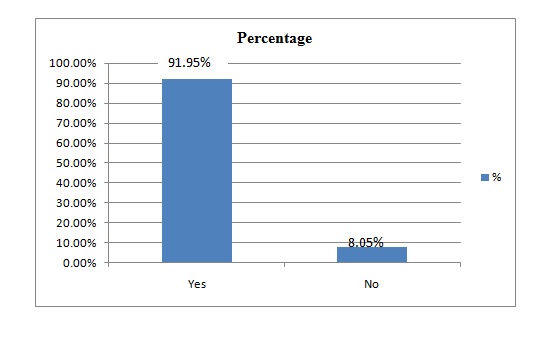

- Involvement of the organization in Carbon Credit Trading

The following description in table 2 shows that the involvement of organizations in Carbon Credit Trading:

Table 2 Involvement of the Organization

|

S. No.

|

Answer

|

Frequency

|

%

|

|

1

|

Yes

|

80

|

91.95%

|

|

2

|

No

|

7

|

8.05%

|

|

3

|

Total

|

87

|

100.0%

|

The above table represents that 91.95% of the respondents says that their organizations are involved in carbon credit trading whereas 8.05% respondents refuse about their involvement in carbon credit trading but are looking forward to get involved in future.

- Benefits gained by organization by implementing carbon credit trading

The following table 3 shows that the various benefits gained by the organizations by implementing carbon credit trading:

|

Table 3 Benefits of Carbon Credit Trading

|

|

|

|

Total

|

|

Improvement in Social Status

|

Reduction in overall cost

|

Additional Revenue

|

Funds for R & D

|

Market Share Value

|

|

Answer

|

Strongly Agree

|

Count

|

34

|

10

|

32

|

12

|

32

|

120

|

|

Expected Count

|

24

|

24

|

24

|

24

|

24

|

|

|

|

% within

|

42.5

|

12.5

|

40

|

15

|

40

|

|

|

Agree

|

Count

|

26

|

8

|

30

|

16

|

30

|

110

|

|

Expected Count

|

22

|

22

|

22

|

22

|

22

|

|

|

|

% within

|

32.5

|

10

|

37.5

|

20

|

37.5

|

|

|

Neutral

|

Count

|

10

|

48

|

8

|

34

|

10

|

110

|

|

Expected Count

|

22

|

22

|

22

|

22

|

22

|

|

|

|

% within

|

12.5

|

60

|

10

|

42.5

|

12.5

|

|

|

Disagree

|

Count

|

8

|

8

|

8

|

10

|

4

|

38

|

|

Expected Count

|

7.6

|

7.6

|

7.6

|

7.6

|

7.6

|

|

|

|

% within

|

10

|

10

|

10

|

12.5

|

5

|

|

|

Strongly Disagree

|

Count

|

2

|

6

|

2

|

8

|

4

|

22

|

|

Expected Count

|

4.4

|

4.4

|

4.4

|

4.4

|

4.4

|

|

|

|

% within

|

2.5

|

7.5

|

2.5

|

10

|

5

|

|

|

Total

|

|

Count

|

80

|

80

|

80

|

80

|

80

|

400

|

|

|

% within

|

20.0%

|

20.0%

|

20.0%

|

20.0%

|

20.0%

|

100.0%

|

- Problem Statement: Carbon credit trading has improved the social status of the organizations.

H0: Carbon credit trading has no effect on the social status of the organizations.

H1: Carbon credit trading has improved the social status of the organizations.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.025

|

|

2

|

HYPOTHESIZED MEAN

|

3.67

|

|

3

|

STANDARD DEVIATION

|

1.0837

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.0719

|

REJECTED

|

Interpretation: Carbon credit trading has improved the social status of the organizations.

- Problem Statement: Carbon credit trading has resulted in decrease in overall cost of meeting the emission reduction targets.

H0:Carbon credit trading has no effect in overall cost of meeting the emission reduction targets.

H1: Carbon credit trading has resulted in decrease in overall cost of meeting the emission reduction targets.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

3.1

|

|

2

|

HYPOTHESIZED MEAN

|

3.67

|

|

3

|

STANDARD DEVIATION

|

0.9949

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

3.6234

|

REJECTED

|

Interpretation: Carbon credit trading has resulted in decrease in overall cost of meeting the emission reduction targets.

- Problem Statement: Carbon credit trading offers additional revenue to the organizations.

H0:Carbon credit trading does not offer any additional revenue to the organizations.

H1: Carbon credit trading offers additional revenue to the organizations.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.05

|

|

2

|

HYPOTHESIZED MEAN

|

3.67

|

|

3

|

STANDARD DEVIATION

|

1.0604

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.1176

|

REJECTED

|

Interpretation: Carbon credit trading offers additional revenue to the organizations.

- Problem Statement: Carbon credit trading helps research and development purpose by providing the funds.

H0: Carbon credit trading does not provide any help to research and development purpose by providing the funds.

H1: Carbon credit trading helps research and development purpose by providing the funds.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

3.175

|

|

2

|

HYPOTHESIZED MEAN

|

3.67

|

|

3

|

STANDARD DEVIATION

|

1.1377

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.7519

|

REJECTED

|

Interpretation: Carbon credit trading helps research and development purpose by providing the funds.

- Problem Statement: Carbon credit trading has improved the organizations’ market share value.

H0: Carbon credit trading has no effect on organizations’ market share value.

H1: Carbon credit trading has improved the organizations’ market share value.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.025

|

|

2

|

HYPOTHESIZED MEAN

|

3.67

|

|

3

|

STANDARD DEVIATION

|

1.0837

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.0719

|

REJECTED

|

Interpretation: Carbon credit trading has improved the organizations’ market share value.

There are lots of benefits gained by the organizations by implementing carbon credit trading. The main benefit of this concept is the improvement in social status of the organizations. Another benefit is the decrease in the overall cost of meeting the emission reduction targets. The carbon credit trading offers additional revenue to the various organizations and they can use these funds for research and development. Also, the overall market share value of the organizations can also be increased by involving the organization in carbon credit trading.

- Challenges associated with implementing carbon credit trading practices in organizations

The following table 4 shows the impact of various challenges associated with implementing carbon credit trading practices in the organizations:

|

|

Table 4 Challenges of Carbon Credit Trading

|

|

|

|

|

|

Total

|

|

|

Taxation Issues

|

Ambiguity

|

Encourages movement towards unsustainable ways

|

Explicit mention of these transactions as exports

|

|

Source of

perverse

incentive

|

|

|

Answers

|

Strongly Agree

|

Count

|

34

|

26

|

12

|

20

|

|

36

|

128

|

|

Expected Count

|

25.6

|

25.6

|

25.6

|

25.6

|

|

25.6

|

|

|

|

% within

|

42.5

|

32.5

|

15

|

25

|

|

45

|

|

|

Agree

|

Count

|

26

|

34

|

18

|

18

|

|

26

|

122

|

|

Expected Count

|

24.4

|

24.4

|

24.4

|

24.4

|

|

24.4

|

|

|

|

% within

|

32.5

|

42.5

|

22.5

|

22.5

|

|

32.5

|

|

|

Neutral

|

Count

|

12

|

16

|

26

|

14

|

|

12

|

80

|

|

Expected Count

|

16

|

16

|

16

|

16

|

|

16

|

|

|

|

% within

|

15

|

20

|

32.5

|

17.5

|

|

15

|

|

|

Disagree

|

Count

|

6

|

4

|

12

|

25

|

|

2

|

50

|

|

Expected Count

|

10

|

10

|

10

|

10

|

|

10

|

|

|

|

% within

|

7.5

|

5

|

15

|

32.5

|

|

2.5

|

|

|

Strongly Disagree

|

Count

|

2

|

0

|

12

|

2

|

|

4

|

20

|

|

Expected Count

|

4

|

4

|

4

|

4

|

|

4

|

|

|

|

% within

|

2.5

|

0

|

15

|

2.5

|

|

5

|

|

|

Total

|

|

Count

|

80

|

80

|

80

|

80

|

|

80

|

400

|

|

|

% within

|

100.0%

|

100.0%

|

100.0%

|

100.0%

|

|

100.0%

|

100.0%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- Problem Statement: Carbon credit trading creates several taxation issues to the organizations.

H0: Carbon credit trading does not create any taxation issues to the organizations.

H1: Carbon credit trading creates several taxation issues to the organizations.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.05

|

|

2

|

HYPOTHESIZED MEAN

|

3.72

|

|

3

|

STANDARD DEVIATION

|

1.0476

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

1.9924

|

REJECTED

|

Interpretation: Carbon credit trading creates several taxation issues to the organizations.

- Problem Statement: Accounting of carbon credit has lot of ambiguity involved in it due to lack of proper accounting standards.

H0: Accounting of carbon credit does not have any ambiguity involved in it due to lack of proper accounting standards.

H1: Accounting of carbon credit has lot of ambiguity involved in it due to lack of proper accounting standards.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.025

|

|

2

|

HYPOTHESIZED MEAN

|

3.72

|

|

3

|

STANDARD DEVIATION

|

0.8511

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.2667

|

REJECTED

|

Interpretation: Accounting of carbon credit has lot of ambiguity involved in it due to lack of proper accounting standards.

- Problem Statement: Carbon credit trading encourages the rich to move towards more unsustainable ways.

H0: Carbon credit trading does not encourage the rich to move towards more unsustainable ways.

H1: Carbon credit trading encourages the rich to move towards more unsustainable ways.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

3.075

|

|

2

|

HYPOTHESIZED MEAN

|

3.72

|

|

3

|

STANDARD DEVIATION

|

1.2528

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

3.2565

|

REJECTED

|

Interpretation: Carbon credit trading encourages the rich to move towards more unsustainable ways.

- Problem Statement: The export of Carbon credit made to the foreign buyers yields some taxes, so there should be explicit mention of these transactions as exports.

H0: The export of Carbon credit made to the foreign buyers yields no tax, so there is no need of explicit mention of these transactions as exports.

H1: The export of Carbon credit made to the foreign buyers yields some taxes, so there should be explicit mention of these transactions as exports.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

3.35

|

|

2

|

HYPOTHESIZED MEAN

|

3.72

|

|

3

|

STANDARD DEVIATION

|

1.2359

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

1.8935

|

ACCEPTED

|

Interpretation: The export of Carbon credit made to the foreign buyers yields no tax, so there is no need of explicit mention of these transactions as exports.

- Problem Statement: Carbon credit stands as a source of perverse incentive to the organizations as well as the country.

H0: Carbon credit does not stand as a source of perverse incentive to the organizations as well as the country.

H1: Carbon credit stands as a source of perverse incentive to the organizations as well as the country.

country.

|

S.No.

|

PARTICULARS

|

VALUE

|

|

1

|

SAMPLE MEAN

|

4.1

|

|

2

|

HYPOTHESIZED MEAN

|

3.72

|

|

3

|

STANDARD DEVIATION

|

1.0677

|

|

Z – Tests

|

|

|

|

|

LEVEL OF SIGNIFICANCE

|

TABLE VALUE

|

Calculated Value

|

H0

|

|

Z

|

5 %

|

1.96

|

2.2511

|

REJECTED

|

Interpretation: Carbon credit stands as a source of perverse incentive to the organizations as well as the country.

In carbon credit trading, there are lots of challenges regarding taxation. The accounting of carbon credit has lot of ambiguity involved in it due to lack of proper accounting standards. This trading also encourages the rich to move towards more unsustainable ways, but the export of carbon credit is made to the foreign buyers’ yields no tax, so there is no need of explicit mention of these transactions as exports.

Conclusion

Carbon credit trading is a concept which is used to reduce the carbon emission level from the atmosphere. Now most of the organizations adopt this concept and earn several types of benefits but they also face some challenges. According to the above research, there are several business sectors which are directly involved in carbon credits trading such as energy supply, transportation, infrastructure, manufacturing industries, agriculture, forestry, waste management, etc. Some companies like Gujarat Fluoro-chemicals Limited (GFL), SRF Limited, Delhi Metro Rail Corporation (DMRC), Jindal Vijaynagar Steel, Kalpatru Power Transmission Ltd. taking lots of benefits from carbon credits trading. The above research is also shows that most of the organizations are taking interest in carbon credits trading. The main benefit which companies earn other than monetary is improvement in social status and market share. Nation’s point of view, the country is benefitted in decreasing the carbon emission level from the atmosphere. This is the foremost benefit which we earn from carbon credits trading. If we take fresh air then lots of problem will automatically resolved. Apart from benefits, there are lots of challenges we face in carbon credits trading. The main challenges are taxation policies, proper accounting standards, documentations regarding export of carbon credits, etc. At last, the carbon credit trading stands as a source of perverse incentive to the organizations as well as to the country.

References: